-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Positioning for Market Risks in 2019

10 December 2018

10 min read

Christopher W. Marx| Global Head—Equity Business Development

Erin Bigley, CFA| Chief Responsibility Officer

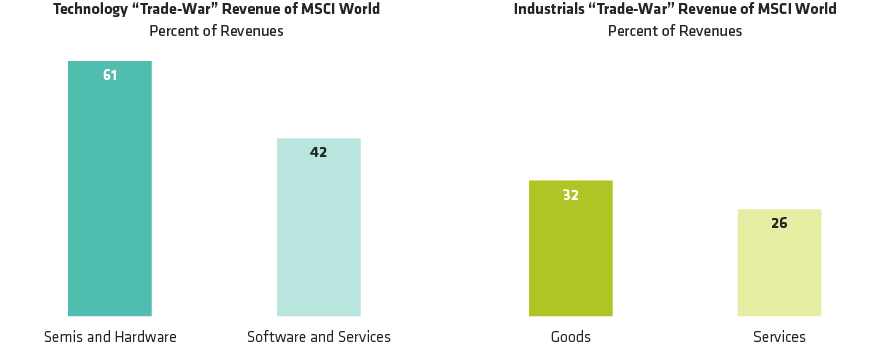

What Industries Are More Exposed to Trade-War Fallout?

As of September 30, 2018

“Trade-war” revenue for US stocks is non-US revenue, and for non-US stocks is US revenue.

Source: FactSet, MSCI and AllianceBernstein (AB)

ECB Has Many Levers to Pull to Support Economic Recovery

Source: AllianceBernstein (AB)

A Rising-Rate Portfolio Soon Outpaces a No-Rate-Rise Portfolio

For illustrative purposes only

Source: US Department of the Treasury and AllianceBernstein (AB)

-

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

About the Authors

Christopher W. Marx is Senior Vice President and Global Head of Equity Business Development. He is responsible for overseeing the firm's team of equity investment strategists and product managers, setting strategic priorities and goals for the global Equities business, developing new products, and engaging with clients to represent market views and investment strategies of the firm. Previously, Marx was a senior investment strategist and a portfolio manager of Equities, and in 2011 he cofounded the Global, International and US Strategic Core Equity portfolios with Kent Hargis. He joined the firm in 1997 as a research analyst covering a variety of industries both domestically and internationally, including chemicals, metals, retail and consumer staples. Marx became part of the portfolio-management team in 2004. Prior to joining the firm, he spent six years as a consultant for Deloitte & Touche and Boston Consulting Group. Marx holds a BA in economics from Harvard University and an MBA from the Stanford Graduate School of Business. Location: New York

Erin Bigley is a Senior Vice President, AB’s Chief Responsibility Officer, and a member of the firm’s Operating Committee and Women’s Leadership Council. In this role, she oversees AB’s responsible investing strategy, including integrating material environmental, social and governance considerations throughout the firm’s research, engagement and investment processes. Bigley joined the firm in 1997 and previously served as a portfolio manager and trader for the global and Canadian bond strategies. She spent two years based in London as the global head of Fixed Income Business Development for institutional clients. Bigley served as a fixed-income senior investment strategist for over a decade, and as head of the strategist team from 2018 to 2021. Prior to taking her current role, she served as head of Fixed Income Responsible Investing, overseeing the Fixed Income team’s responsible investing strategy. Bigley holds a BS in civil engineering from Villanova University and an MBA from the Massachusetts Institute of Technology’s Sloan School of Management. She is a CFA charterholder. Location: New York

More For You

World Economy to Continue Rebalancing in 2025

The range of potential economic outcomes is wide, but a solid starting point suggests resilience.

Mapping Out the 2025 Investment Landscape Across Asset Classes

Global markets will face powerful disruptive forces next year. How can investors prepare in fixed-income, equity and alternative investment strategies?

Five Themes for ’25 and their SAA Implications for US Equities, TIPS and Crypto

This note outlines five investment themes for 2025. These are not necessarily trades for the coming year, but rather issues that asset owners need to think about—even if some implications are longer term. They are topics which we believe necessitate a change in investors’ expectations and in their asset allocations.