-

Past performance, historical and current analyses, and expectations do not guarantee future results. There can be no assurance that any investment objectives will be achieved. The information contained here reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion in this material will be realized. Past performance does not guarantee future results. The views expressed here may change at any time after the date of this publication. This document is for informational purposes only and does not constitute investment advice. AllianceBernstein L.P. does not provide tax, legal or accounting advice. It does not take an investor’s personal investment objectives or financial situation into account; investors should discuss their individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer or solicitation for the purchase or sale of any financial instrument, product or service sponsored by AB or its affiliates.

The views expressed herein do not constitute research, investment advice, or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

What’s Old Is New Again

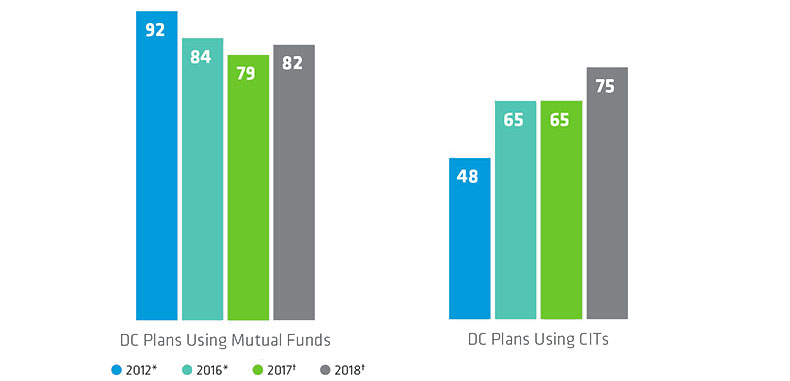

Collective Investment Trusts Reduce DC Plan Costs

Historical and current analyses do not guarantee future results.

*Callan Associates, 2017 Defined Contribution Trends Survey

†Callan Associates, 2019 Defined Contribution Trends Survey

Jennifer DeLong is a Senior Vice President, Managing Director and Head of Defined Contribution, responsible for leading AB’s defined contribution business in North America. She oversees product management and development, marketing, participant communications, and client services for the firm’s institutional custom target-date and lifetime income solution clients. Additionally, DeLong is responsible for firm’s Collective Investment Trust business and is President of the AllianceBernstein Trust Company. Since joining AB in 1999, she has held various senior client relationship management, product management and marketing roles, all primarily focused on defined contribution, 529 college savings plans and sub-advisory insurance services for both institutional and retail clients. Before joining the firm, DeLong worked in various sales, marketing and client relationship management roles for both small and mega-sized defined contribution plans. She holds a BS in business management with a minor in international business from The College of New Jersey, as well as FINRA Series 6 and 63 licenses. Location: New York

More For You

Engaging up front with four key workstreams may smooth the process of adding a solution.

For DC plan sponsors, developing a short list of income solutions is a good first step.

Understanding investor differences may help DC plan sponsors improve communications—and outcomes—for more than just the “average” participant.