-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

Asian Stocks

Value Appeal Revealed in Coronavirus Recovery

12 May 2020

4 min read

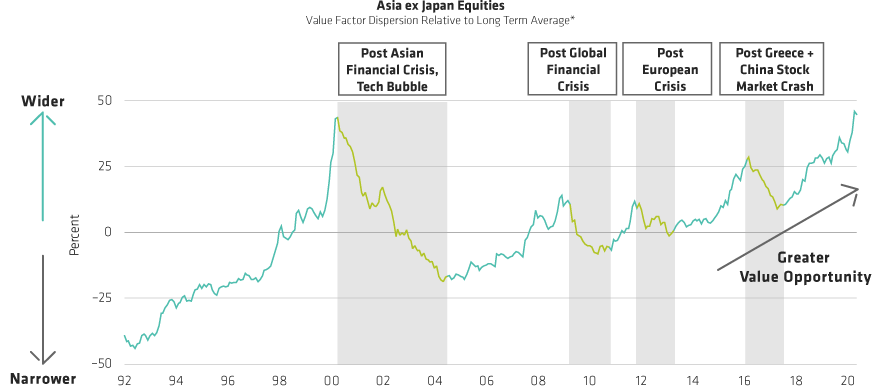

Do Wide Valuation Spreads in Asia Point to Post-Pandemic Rebound?

Analysis provided for illustrative purposes only and is subject to revision.

*Based on the AB Asia ex Japan universe of stocks. Valuation spread reflects the difference between the highest and lowest quintiles of stocks, and is calculated using a cross-sectional standard deviation of AB’s proprietary valuation metrics. Long-term average since 1992. Value factors used for the calculation include price/book, price/forward earnings, price/earnings, price/cash earnings and price/sales.

As of April 30, 2020

Source: Bloomberg, FactSet, MSCI, Thomson Reuters I/B/E/S, Worldscope and AllianceBernstein (AB)

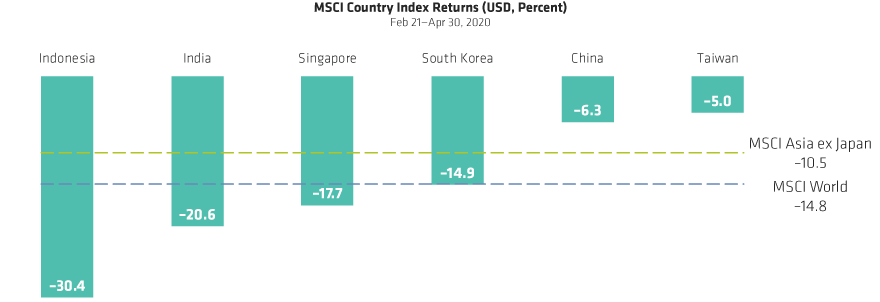

Asian Equity Markets Reflect Coronavirus Recovery Divergence

Historical performance does not guarantee future results.

As of April 30, 2020

Source: FactSet, MSCI and AllianceBernstein (AB)

Memory Market: Improving Supply-Demand Dynamics

*Based on the contract price for PC DRAM (4GB DDR4)

As of December 31, 2019

Source: Citibank, DRAMeXchange, FactSet and AllianceBernstein (AB)

About the Author