-

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

ECB’s Surprise Taper Decision Comes with Economic Risk

16 March 2022

4 min read

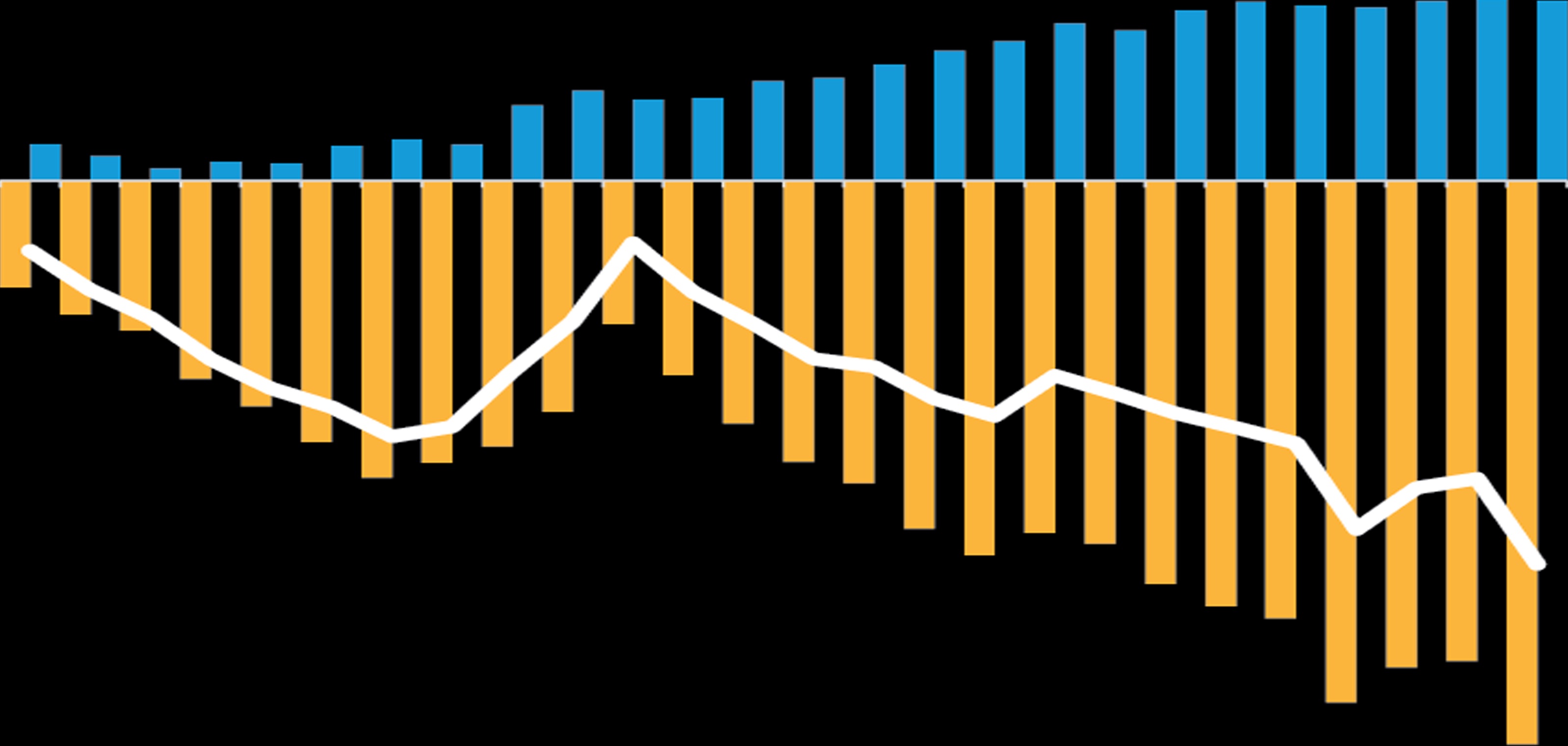

Euro-Area Real Incomes Are Already Stagnant

Nominal and Inflation-Adjusted Paycheck, Year-over-Year Percent Change

Past performance does not guarantee future results.

Through February 28, 2022

Source: Refinitiv Datastream

Strong PMI Doesn’t Yet Reflect War and Energy Price Spike

Eurozone Manufacturing and Services Purchasing Managers’ Index

Past performance does not guarantee future results.

Through February 28, 2022

Source: Refinitiv Datastream

About the Authors

Eric Winograd is a Senior Vice President and Director of Developed Market Economic Research. He joined the firm in 2017. From 2010 to 2016, Winograd was the senior economist at MKP Capital Management, a US-based diversified alternatives manager. From 2008 to 2010, he was the senior macro strategist at HSBC North America. Earlier in his career, Winograd worked at the Federal Reserve Bank of New York and the World Bank. He holds a BA (cum laude) in Asian studies from Dartmouth College and an MA in international studies from the Paul H. Nitze School of Advanced International Studies. Location: New York

More For You

European Tariff Talks: Does the US Hold All the Cards?

Negotiating with one key trade partner is tough enough. Negotiating with two is highly testing.

Capital Markets Outlook 2Q 2025: At the Intersection of Fear and Hope

After a disappointing quarter and a bout of tariff turmoil, what does the opportunity set look like?

Anatomy of a US Treasury Sell-Off

What triggered April’s Treasury sell-off? What’s next? And how should investors manage duration risk?