-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Fragile No More

Emerging Opportunities in Currencies and Bonds

October 26, 2016

3 min read

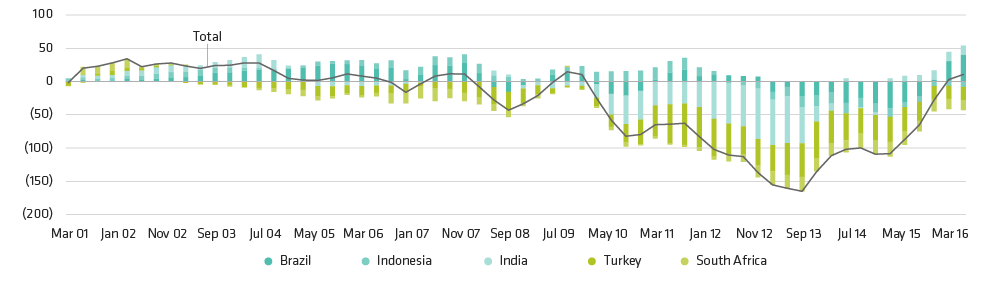

On the Mend: FDI Shoring Up Fragile Five’s Balance Sheets

Fragile Five Basic Balance* (USD)

As of June 30, 2016

*Basic balance = FDI plus current account balance

Source: Haver Analytics

About the Author

Christian DiClementi is a Senior Vice President and Lead Emerging Market Debt Portfolio Manager at AB. He is also a member of the Global Fixed Income, Absolute Return and Income portfolio-management teams, and oversees emerging-market investments across AB’s suite of fixed-income products. DiClementi joined the firm in 2003. Prior to becoming a member of the Emerging Market Debt portfolio-management team in 2013, he served as a member of AB’s Economic Research Group, focusing mainly on sovereign fundamental research for the Caribbean, Central American and Latin American regions. Previously, DiClementi worked as an analyst in the firm’s Quantitative Research Group, with an emphasis on global sovereign return and risk modeling, and as an associate portfolio manager responsible for municipal bond portfolios. He holds a BS in mathematics (summa cum laude) from Fairfield University. Location: New York

More For You

What Does the DeepSeek Halo Teach Us About Chinese Stocks?

The AI breakthrough spotlights some of China’s distinctive features that deserve closer attention from investors.

China Seeks Wiggle Room for Growth in Year of the Snake

China’s efforts to steer between domestic and international growth challenges in 2025 could be good for bond investors.

How to Invest in Emerging Market Equities as New US Policies Bite

Not all companies in emerging markets will be hurt by President Trump’s agenda. Here’s what equity investors should look for.