-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Why It Pays to Keep an Eye on the Credit Cycle

Jan 27, 2016

3 min read

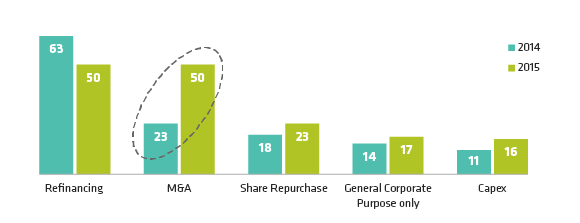

M&A Activity On The Rise

Issuance Elevated by Large-Cap M&A Use of Proceeds (Percent)

As of December 31, 2015

Source: Deutsche Bank

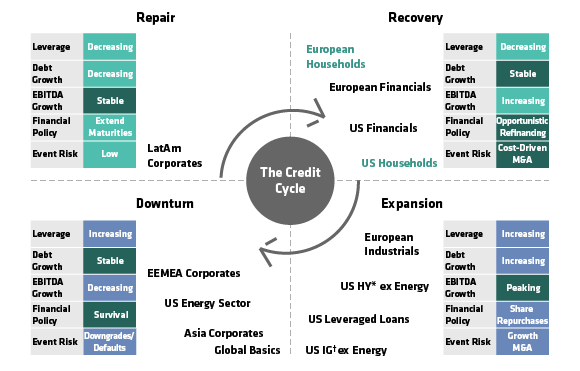

Credit Cycle Continues To Advance, But Stage Varies Widely By Sector

As of December 31, 2015

*High yield

†Investment grade

Source: AB

About the Authors