-

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

Balanced Bond Strategies Aren't Broken. Here's Why.

06 July 2020

3 min read

Treasuries Provide Diversification When It’s Needed Most

10-Year Treasury Yield vs. High-Yield Spread: Six-Month Rolling Correlation of Daily Moves

Through May 31, 2020

High-yield spreads are option adjusted.

Source: Bloomberg Barclays and AllianceBernstein (AB)

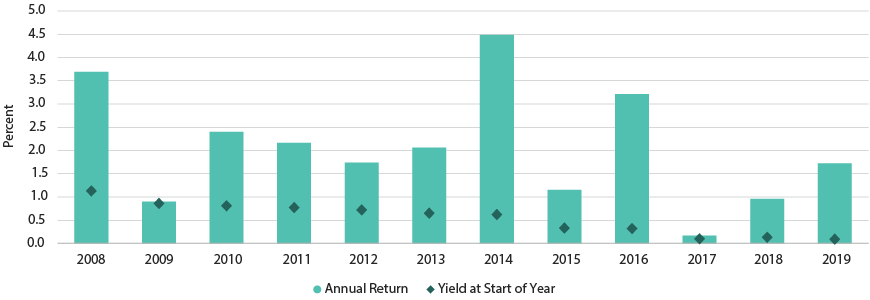

Low Yields Don’t Always Mean Low Returns

10-Year Japanese Government Bonds: Yield and Return

Through December 31, 2019

Compares yield at start of year to that year’s total return

Source: Bloomberg Barclays and AllianceBernstein (AB)

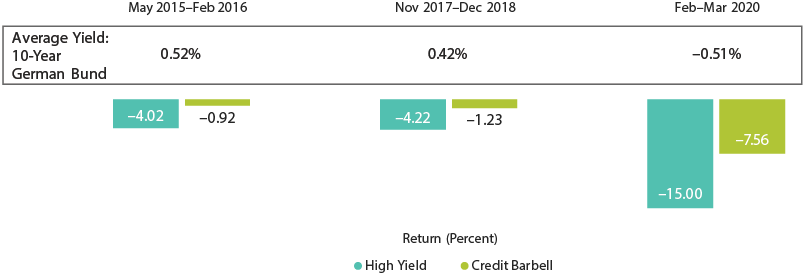

Barbell Mitigated Downside Even When Yields Were Low or Negative

Euro-Area Downturns: 2015–2020

As of June 30, 2020

High yields represented by Bloomberg Barclays Euro High Yield Index; credit barbell is represented by a hypothetical naive barbell of 50% Bloomberg Barclays Euro

High Yield Index and 50% 10-year German bunds.

Source: Bloomberg Barclays and AllianceBernstein (AB)

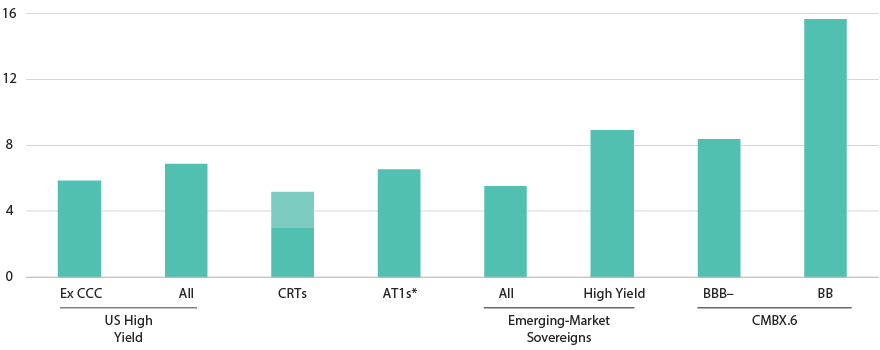

Diversifying Beyond US High Yield Can Boost Income

Yield

CRT yields as of June 26, 2020; all other data as of June 30, 2020

*European bank AT1s

CMBX yields are loss adjusted. CRT yields are expressed as ranges.

Source: Bank of America ML, Bloomberg Barclays, IHS Marki, J.P. Morgan and AllianceBernstein (AB)

About the Authors