-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Why Passive Investing Isn’t a Panacea

03 April 2018

3 min read

Richard A. Brink, CFA| Market Strategist—Client Group

Walt Czaicki, CFA | Senior Investment Strategist—Equities

Scott Krauthamer, CFA, CAIA| Global Head—Product Management & Strategy

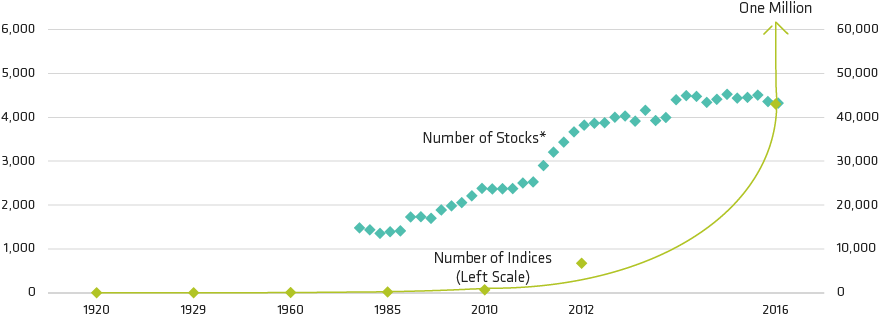

There Are Many More Indices than Stocks in the World Today

Through December 31, 2016

Historical analysis does not guarantee future results

*Of the approximately 43,000 stocks globally, it's estimated that roughly 2,300 can be invested in broadly.

Source:Bernstein

About the Authors

Richard A. Brink is a Senior Vice President and Market Strategist in the Client Group. Previously, he served as a managing director in the Alternatives and Multi-Asset Group. Prior to that role, Brink was a senior portfolio manager in Fixed Income, and before that an investment director for fixed-income investments within the Global Retail Investments Group. Before joining AB in 2004, he was senior product manager at the Dreyfus Corporation, covering both retail and institutional fixed-income offerings. Brink was previously a senior trainer, dealing primarily with the design and delivery of product training to financial advisors and mutual fund sales representatives. He holds a BS in applied mathematics and economics from Stony Brook University, and is a CFA charterholder. Location: New York

Walt Czaicki serves as a Senior Vice President and Senior Investment Strategist for Equities at AB. He rejoined the firm in 2015 and has been in the investment-management industry since 1986. Czaicki's roles have ranged from a fundamental equity research analyst and portfolio manager to chief investment officer. Prior to rejoining AB, he worked on the buy side for a Regions Financial predecessor organization, as well as at Commerce Trust Company and Bank of America. Czaicki holds a BSBA in finance and an MBA, both from Saint Louis University. He is a CFA charterholder. Location: Dallas

Scott Krauthamer is a Senior Vice President and Global Head of Product Management & Strategy, overseeing AB's global investment products across the firm's equity, fixed income and multi-asset strategies. Prior to joining the firm, he held a variety of investment and product-management roles at Legg Mason, U.S. Trust, Bank of America and J.P. Morgan Private Bank. Krauthamer started his career as an analyst at J.P. Morgan in 1998, and his financial-services experience spans investment-management, quantitative analysis, marketing and business development. He holds a BS in finance and management information systems from the State University of New York, Albany, and is a CFA charterholder and a CAIA designee. Location: Nashville

More For You

Six Impossible Things Before Breakfast?

The unwinding of “Trump trades,” a spike in volatility and the outperformance of European versus US equities have sparked debate about whether this is a tactical shift or the beginnings of a longer bearish trajectory for markets.

Europe: The Next Frontier in Asset-Based Finance

Banks’ retreat is creating opportunity for investors.

A Higher Inflation Future and the Need for Real Assets

The risk of higher equilibrium inflation is a key marker of the notion that investors face a new regime. Recent policy announcements have lent more weight to the idea that the path of inflation might be upward. In this note we focus on the disparate forces that imply a higher long-term level of inflation.