Still, the true amount of exposure to international trade goes beyond where a company’s customers are. Further, it varies widely among SMID industries and individual companies—and those variations often require a bit of digging to tease out. Buying an exchange-traded fund that tracks a small-cap index may not offer investors as much protection from protectionism as they think.

From Banks to Truckers

To understand why, think about the banking industry. Banks in the SMID space are primarily regional players, and domestic customers make up the vast bulk of their loan portfolios. But it’s important to know who exactly those customers are. What if they’re construction equipment manufacturers that are being squeezed by rising steel and aluminum prices because of US-imposed tariffs? A regional bank may not take a hit overnight, but if too many manufacturers run into problems and fall behind on their payments, the banks’ loan performance would eventually suffer. The same would go for a rural bank that lends to farmers who must now contend with heavy Chinese tariffs on some of their products.

American trucking companies are another group that may be more vulnerable to global trade disruptions than they first appear. Their routes are, by definition, in the US. But what they’re carrying matters as much as where they’re carrying it. Tariffs tend to raise prices across the board, which in turn raises the risk that consumers and businesses will choose to make do with less rather than spend more. That, in turn, could leave truckers with less freight to haul.

New Risks to Consumer Spending

Consumer spending could be another pain point for all kinds of businesses in a trade war. A restaurant chain based entirely in the US may depend primarily on American appetites for its daily bread. But if, for instance, the American workers on the factories and farms mentioned above lose their jobs or get their hours cut, they aren’t likely to stop by for a bite quite as often.

Investors should be mindful of these nuances and be wary of claims that a trade war is “good” for SMID stocks. The truth is that a trade war will cut deep for companies of all sizes, and it’s important to understand the specific and relative risks to each individual stock in a portfolio.

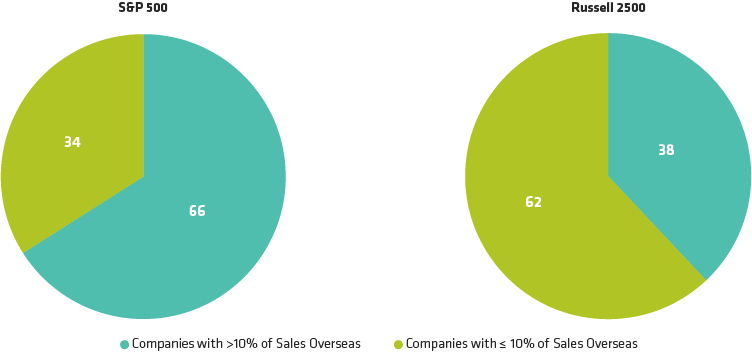

At the same time, we believe that SMID stocks are a good category in which to hunt for companies with relatively little international exposure. But the key word is hunt. Despite the Russell 2500’s recent positive performance, this isn’t the time to simply follow the index. Careful and active consideration of each firm’s individual exposure to global trade gyrations—and potential second-order effects—is the only way to ensure that positions in smaller stocks can thrive through a larger trade war.

.png)