-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Income Investing When (Trade) Tensions Run High

11 September 2019

3 min read

Mortgage-Based Assets Weather Rougher Trade Winds

Through May 31, 2019

Historical analyses do not guarantee future results. CRTs and CMBS are represented by bonds (including CMBX.6 holdings) held in those sectors in an AB-managed fixed-income portfolio, and are therefore not intended to represent a generally accepted proxy/benchmark for these markets. For illustrative purposes only.

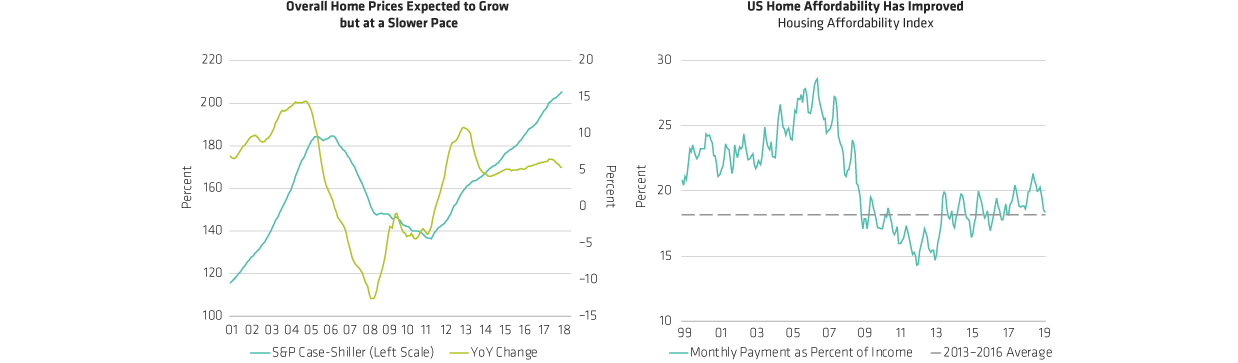

US Housing Market Outlook Still Solid

Left display through January 1, 2019; right display through February 28, 2019.

Historical and current analyses do not guarantee future results.

Source: Freddie Mac, Morgan Stanley, National Association of Realtors, S&P Case-Shiller, US Census Bureau and AllianceBernstein (AB)

About the Author