-

Past performance, historical and current analyses, and expectations do not guarantee future results. There can be no assurance that any investment objectives will be achieved. The information contained here reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion in this material will be realized. Past performance does not guarantee future results. The views expressed here may change at any time after the date of this publication. This document is for informational purposes only and does not constitute investment advice. AllianceBernstein L.P. does not provide tax, legal or accounting advice. It does not take an investor’s personal investment objectives or financial situation into account; investors should discuss their individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer or solicitation for the purchase or sale of any financial instrument, product or service sponsored by AB or its affiliates.

The views expressed herein do not constitute research, investment advice, or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

Fixed Income

Bracing Your Portfolio for Tough Conditions in 2020

As of December 31, 2019

Past performance and historical and current analysis do not guarantee future results.

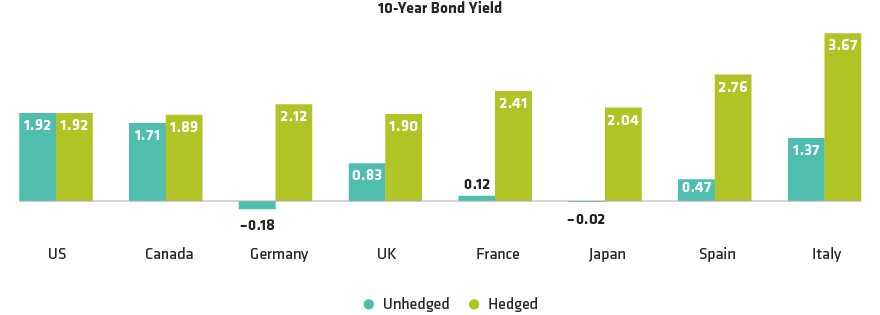

Hedge: A hedge is an investment to reduce the risk of adverse price movements in an asset, such as taking an offsetting position in a related security.

Source: Bloomberg Barclays and AllianceBernstein (AB)

Monika Carlson is a Managing Director, Senior Investment Strategist, and Head of the Income and Systematic platforms for the Fixed Income Business Development team. She is responsible for leading a team of investment strategists and product managers and for driving growth efforts on AB’s fixed-income platform. Additionally, as part of her client-facing role, Carlson represents AB’s market views and portfolio strategies to clients, prospects and consultants globally. She has held several roles at AB, including as the head of the Global Offshore Retail Platform in Product Management. Prior to joining AB in 2007, Carlson worked at Neuberger Berman. She holds a BBA in finance from Baruch College at the City University of New York and is a CFA charterholder. Location: New York

Scott DiMaggio is a Senior Vice President, Head of Fixed Income and a member of the Operating Committee. As Head of Fixed Income, he is responsible for the management and strategic growth of AB’s fixed-income business and investment decisions across the department. DiMaggio has previously served as director of Global Fixed Income and continues to be a portfolio manager across numerous multi-sector and multi-currency strategies. Prior to joining AB’s Fixed Income portfolio-management team, he performed quantitative investment analysis, including asset-liability, asset-allocation, return attribution and risk analysis for the firm. Before joining the firm in 1999, DiMaggio was a risk management market analyst at Santander Investment Securities. He also held positions as a senior consultant at Ernst & Young and Andersen Consulting. DiMaggio holds a BS in business administration from the State University of New York, Albany, and an MS in finance from Baruch College. He is a member of the Global Association of Risk Professionals and a CFA charterholder. Location: New York

Gershon Distenfeld is a Senior Vice President, Director of Income Strategies and a member of the firm’s Operating Committee. He is responsible for the portfolio management and strategic growth of AB’s income platform with almost $60B in assets under management. This includes the multiple-award-winning Global High Yield and American Income portfolios, flagship fixed-income funds on the firm’s Luxembourg-domiciled fund platform for non-US investors. Distenfeld also oversees AB’s public leveraged finance business. He joined AB in 1998 as a fixed-income business analyst and served in the following roles: high-yield trader (1999–2002), high-yield portfolio manager (2002–2006), director of High Yield (2006–2015), director of Credit (2015–2018) and co-head of Fixed Income (2018–2023). Distenfeld began his career as an operations analyst supporting Emerging Markets Debt at Lehman Brothers. He holds a BS in finance from the Sy Syms School of Business at Yeshiva University and is a CFA charterholder. Location: Nashville

More For You

Efforts to secure supply chains and energy sources are creating powerful and enduring themes for equity investors—even in these turbulent times.

Following a defensive equity playbook can help investors prepare for market volatility in a year of heightened uncertainty.

We started the year having discussions with a large number of chief investment officers (CIOs) and allocators. In this short note, we reflect on the key common messages that came out of those discussions, points of consensus and important open questions for the outlook. We reflect on how those perspectives overlap with our view that a change in macro regime is the most likely description of the outlook. There was strong agreement among investors on a positive view for risk assets and an overweight position in the US. The area of most agreement in terms of where to increase allocations was private assets, especially private debt. We discuss the key issues that investors have raised across equities, fixed income and alternative assets, and also their views on crypto.