-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Don’t Rely on Cheap Oil to Power Equity Markets

03 January 2019

3 min read

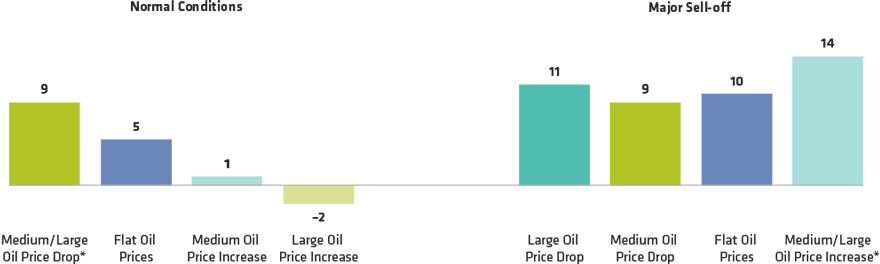

When Oil Prices Fell Below a Critical Threshold, an Uptick in Prices Boosted Returns

One-Month Forward Equity Returns (%)

As of November 14, 2018

The colored bars represent the path of West Texas Intermediate oil prices over the past 12 months. A “large” drop or increase is between 1.5 and 2.5 standard deviations from the mean, a “medium” drop or increase is between 0.5 and 1.5 standard deviations from the mean, and flat is between –0.5 and 0.5 standard deviations from the mean. A “major selloff” is defined as the point when oil prices dip 15% below their five-year average, and normal conditions are anything above that.

*Due to a small number of instances of a large move in oil prices under these two scenarios, the medium and large categories were combined into one.

Source: AllianceBernstein (AB)

About the Author

Sharat Kotikalpudi is the Director of Quantitative Research in the Multi-Asset Solutions Group at AB, specializing in systematic macro strategies; he leads the group's quantitative research in directional and cross-sectional strategies across developed and emerging markets within equity futures, currencies, rates and commodities. He is also a Portfolio Manager of AB Systematic Macro. Kotikalpudi joined AB in 2010 as a quantitative analyst on the Dynamic Asset Allocation team, where he helped to design and develop the quantitative toolset used in the group’s asset-allocation strategies. He holds a BE in electronics and communication engineering from the Manipal Institute of Technology, India, an MA in mathematics of finance from Columbia University and a PGDM from the Indian Institute of Management Calcutta. Location: New York

More For You

Six Impossible Things Before Breakfast?

The unwinding of “Trump trades,” a spike in volatility and the outperformance of European versus US equities have sparked debate about whether this is a tactical shift or the beginnings of a longer bearish trajectory for markets.

Europe: The Next Frontier in Asset-Based Finance

Banks’ retreat is creating opportunity for investors.

A Higher Inflation Future and the Need for Real Assets

The risk of higher equilibrium inflation is a key marker of the notion that investors face a new regime. Recent policy announcements have lent more weight to the idea that the path of inflation might be upward. In this note we focus on the disparate forces that imply a higher long-term level of inflation.