-

For investment professional use only. Not for inspection by, distribution or quotation to, the general public.

Exceeding Expectations in the First Three years

07 June 2021

16 min read

Author

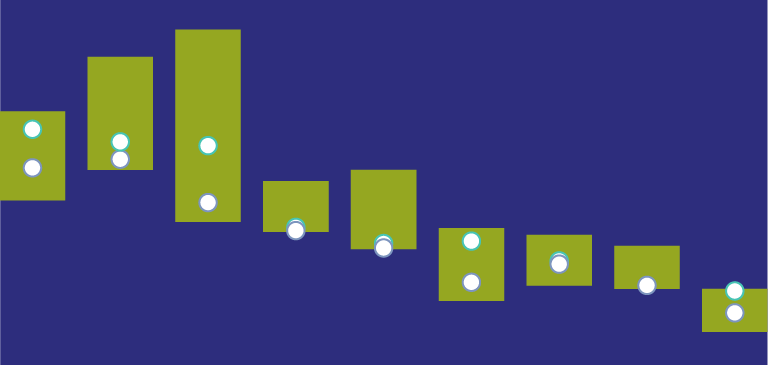

AB Financial Credit Portfolio: Historical Top 10 Issuers

Dynamic Security Selection Based on Relative Value

Historical analysis does not guarantee future results.

The colour is used to group the issuers by country. References to specific securities are presented to illustrate the application of our investment philosophy only and are not to be considered recommendations by AB. The specific securities identified and described do not represent all of the securities purchased, sold or recommended for the Fund, and it should not be assumed that investments in the securities identified were or will be profitable

As of 31 December 2020

Source: AB

AT1 Captured All the Equity Upside

And Limited Setbacks or Performed Positively on the Downside

Historical analyses do not guarantee future returns.

As of 31 December 2020

Source: Bloomberg Barclays

Fund Facts

| CUMULATIVE RETURN INCEPTION TO 17 MAY 2021 | CALENDAR YEAR RETURN 2020 | CALENDAR YEAR RETURN 2019 | CUMULATIVE RETURN 1 JANUARY 2018 TO 14 MAY 2018 | ||

|---|---|---|---|---|---|

| AB Financial Credit Portfolio - S1 Share class | LU1808993833 | 31.9 | 8.6 | 22.1 | -3.7 |

| AB Financial Credit Portfolio - S1 Share class | LU1808993833 | 31.9 | 8.6 | 22.1 | -3.7 |

| Benchmark: Three-Month LIBOR | 5.2 | 1.0 | 2.54 | 1.3 | |

| BB Global COCO Tier 1 Index (USD HEDGED) | H30944US | 28.6 | 7.5 | 20.4 | -3.2 |

| BB European AT1 Index (USD HEDGED) | H31415US | 29.1 | 7.9 | 20.9 | -3.7 |

| BAML COCO index | COCO | 26.0 | 10.2 | 17.4 | -4.9 |

| PIMCO Capital Securities Fund | IE00B6VH4D24 | 23.2 | 6.3 | 17.4 | -4.0 |

| Algebris Financial Credit Fund | IE00BK017B22 | 30.4 | 12.9 | 19.3 | -5.3 |

| GAM Star Credit Opportunities Fund | IE00BDT87D79 | 17.2 | 4.1 | 16.9 | -5.6 |

| Invesco AT1 ETF | AT1 LN Equity | N/A | 8.8 | 18.1 | N/A |

| Bluebay Financial Capital Bond Fund | LU1720194635 | 31.0 | 12.4 | 21.8 | -7.6 |

| SwissCanto CoCo Bond Fund | LU0899937410 | 24.7 | 3.6 | 22.2 | -3.9 |

| CS Coco fund USD | LU2001707251 | N/A | 6.1 | N/A | N/A |

| Jupiter Financial Contingent Capital Fund (ex-OM, ex-Merian) | IE00BF47CX89 | 31.4 | 9.2 | 23.8 | -5.2 |

| Goldman Sachs CoCos & Capital Securities | LU1057459742 | N/A | N/A | 16.0 | -1.6 |

| Edmond de Rothschild Financial Bond Fund | FR0011781210 | 17.0 | 4.6 | 13.6 | -2.7 |

| Robeco Financial Institutions Bonds | LU1117477098 | 18.9 | 4.4 | 15.2 | -1.5 |

| Fonditalia Financial Credit Bond (Fideuram AM/ Algebris) | FOFICBS LX Equity | 16.0 | 7.9 | 14.0 | -6.8 |

| Lyxor Wells Capital Financial Credit Fund | IE00BZ1N8H52 | N/A | 4.9 | 13.9 | N/A |

| Wisdom Tree AT1 ETF | IE00BFNNN012 | N/A | 7.8 | 18.6 | N/A |

| 06/16 –05/17 | 06/17 –05/18 | 06/18 –05/19 | 06/19 –05/20 | 06/20 –05/21 | |

|---|---|---|---|---|---|

| AB Financial Credit Portfolio - S1 Share class (USD) | - | - | 7.2 | 6.1 | 19.9 |

| Benchmark: Three-Month LIBOR | 0.8 | 1.5 | 2.5 | 2.2 | 0.3 |

| Relative Returns | - | - | 4.6 | 3.9 | 19.7 |

-

INVESTMENT RISKS TO CONSIDER

The value of an investment can go down as well as up and investors may not get back the full amount they invested. Past performance does not guarantee future results.

Some of the principal risks of investing in the Portfolio include:

-

Emerging-markets risk: Where the Portfolio invests in emerging markets, these assets are generally smaller and more sensitive to economic and political factors, and may be less easily traded, which could cause a loss to the Portfolio.

-

Focused portfolio risk: Investing in a limited number of issuers, industries, sectors or countries may subject the Portfolio to greater volatility than one invested in a larger or more diverse array of securities.

-

Allocation risk: The risk that the allocation of investments between growth and value companies may have a more significant effect on the Portfolio’s Net Asset Value (NAV) when one of these strategies is not performing as well as the other. In addition, the transaction costs of rebalancing the investments may, over time, be significant.

-

Smaller capitalization companies risk: Investment in securities of companies with relatively small market capitalizations may be subject to more abrupt or erratic market movements because the securities are typically traded in lower volume and are subject to greater business risk.

-

Derivatives risk: The Portfolio may include financial derivative instruments. These may be used to obtain, increase or reduce exposure to underlying assets and may create gearing; their use may result in greater fluctuations of the net asset value.

-

OTC derivatives counterparty risk: Transactions in over-the-counter (OTC) derivatives markets may have generally less governmental regulation and supervision than transactions entered into on organized exchanges. These will be subject to the risk that its direct counterparty will not perform its obligations and that the Portfolio will sustain losses.

-

Equity securities risk: The value of equity investments may fluctuate in response to the activities and results of individual companies or because of market and economic conditions. These investments may decline over short- or long-term periods.

-

Lower-rated and unrated instruments risk: These securities are subject to a greater risk of loss of capital and interest, and are usually less liquid and more volatile. Some investments may be in high-yielding fixed-income securities, so the risk of depreciation and capital losses may be unavoidable

-

Sovereign debt obligations risk: The risk that government issued debt obligations will be exposed to direct or indirect consequences of political, social and economic changes in various countries. Political changes or the economic status of a country may impact the willingness or ability of a government to honour its payment obligations.

-

Corporate debt obligations risk: The risk that a particular issuer may not fulfill its payment and other obligations. In addition, an issuer may experience adverse changes to its financial position or a decrease in its credit rating resulting in increased debt obligation price volatility and negative liquidity. There may also be a higher risk of default.

-

Contingent convertible bonds’ (CoCos) Risk: In addition to those risks generally associated with debt securities, including subordinated debt securities and hybrid debt securities, CoCos are subject to certain additional risks on the occurrence of a pre-determined event resulting in conversion to an issuer’s equity or write-down of principal.

-

These and other risks are described in the Portfolio’s Prospectus and Key Investor Information Document (KIID).

-

The Portfolio is meant as a vehicle for diversification and does not represent a complete investment program. Prospective investors should read the Prospectus carefully and discuss risks and the Portfolio’s fees and charges with their financial advisor to determine if the investment is appropriate for them.

-

Important Information

The information contained here reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion in this material will be realized. This document has been approved by AllianceBernstein Limited, an affiliate of AllianceBernstein L.P.

References to specific securities are presented to illustrate the application of our investment philosophy only and are not to be considered recommendations by AB. The specific securities identified and described do not represent all of the securities purchased, sold or recommended for the Portfolio, and it should not be assumed that investments in the securities identified were or will be profitable.

The AB Financial Credit Portfolio is a portfolio of AB SICAV I, an open-ended investment company with variable capital (société d’investissement à capital variable) incorporated under the laws of the Grand Duchy of Luxembourg.

The sale of AB funds may be restricted or subject to adverse tax consequences in certain jurisdictions. This financial promotion is directed solely at persons in jurisdictions where the funds and relevant share class are registered or who may otherwise lawfully receive it. Before investing, investors should review the Fund’s full Prospectus, together with the Fund’s KIID and the most recent financial statements. Copies of these documents, including the latest annual report and, if issued thereafter, the latest semi-annual report, may be obtained free of charge from AllianceBernstein (Luxembourg) S.à r.l. by visiting www.alliancebernstein.com, or in printed form by contacting the local distributor in the jurisdictions in which the funds are authorised for distribution.

-

Note to Readers in the United Kingdom: This information is issued by AllianceBernstein Limited, 60 London Wall, London EC2M 5SJ. Registered in England, No. 2551144. AllianceBernstein Limited is authorised and regulated in the UK by the Financial Conduct Authority (FCA – Reference Number 147956).

-

Note to Readers in Europe: This information is issued by AllianceBernstein (Luxembourg) S.à r.l. Société à responsabilité limitée, R.C.S. Luxembourg B 34 305, 2-4, rue Eugène Ruppert, L-2453 Luxembourg. Authorised in Luxembourg and regulated by the Commission de Surveillance du Secteur Financier (CSSF).

-

Note to Readers in Austria and Germany: Local paying and information agents: Austria—UniCredit Bank Austria AG, Rothschildplatz 1, 1020 Vienna; Germany—ODDO BHF Aktiengesellschaft, Bockenheimer Landstrasse 10, 60323 Frankfurt am Main.

-

Note to Readers in Switzerland: This document is issued by AllianceBernstein Schweiz AG, Zürich, a company registered in Switzerland under company number CHE-306.220.501. AllianceBernstein Schweiz AG is authorised and regulated in Switzerland by the Swiss Financial Market Supervisory Authority (FINMA) as a distributor of collective investment schemes. Swiss Representative & Swiss Paying Agent: BNP Paribas Securities Services, Paris, Succursale de Zürich. Registered office: Selnaustrasse 16, 8002 Zürich, Switzerland, which is also the place of performance and the place of jurisdiction for any litigation in relation to the distribution of shares in Switzerland. The Prospectus, the KIIDs, the Articles or management regulations, and the annual and semi-annual reports of the concerned fund may be requested without cost at the offices of the Swiss representative.

-

The [A/B] logo is a service mark of AllianceBernstein and AllianceBernstein® is a registered trademark used by permission of the owner, AllianceBernstein L.P.

About the Author

Steve Hussey is a Senior Vice President and Head of Developed-Market Global Banks Research, covering banks in the US, Canada, Europe, Japan and Australia. Prior to joining the firm in 2000, Hussey spent six years at credit rating agency Fitch IBCA, where he was a director, responsible for the Spanish and Latin American banking sectors. He holds a BSc in business economics and accounting, and an MSc in international banking and finance from the University of Southampton (UK). Location: London

More For You

What's in Store for US Insurers in 2023?

US insurance investors enter 2023 facing a less- than-stellar macro environment as well as looming regulatory change. There are opportunities, but it will take selectivity and flexibility to capitalize on them.

Higher Yields Expand Income Options for Multi-Asset Investors

For years, income has been a challenge for many investors, but the yield landscape has improved somewhat since early 2022.

Euro High Yield Demands a Second Look from Investors

With AAA-rated euro government bond yields still negative out to 20 years' maturity, European bond investors seeking income and return potential must consider higher-yielding alternatives.