-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

Can US Stock Investors Rely on Earnings Growth?

February 03, 2020

3 min read

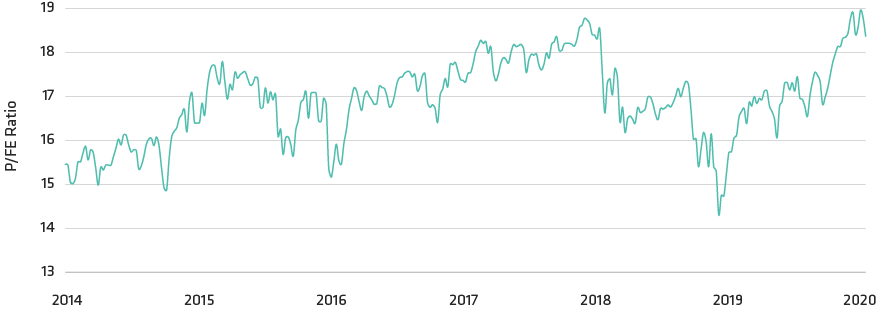

US Stock Valuations Recovered in 2019

S&P 500: Price/Forward Earnings

Past performance and current analyses do not guarantee future results.

Through January 31, 2020

Based on consensus operating earnings estimates for the next 12 months.

Source: Bloomberg, S&P and AllianceBernstein (AB)

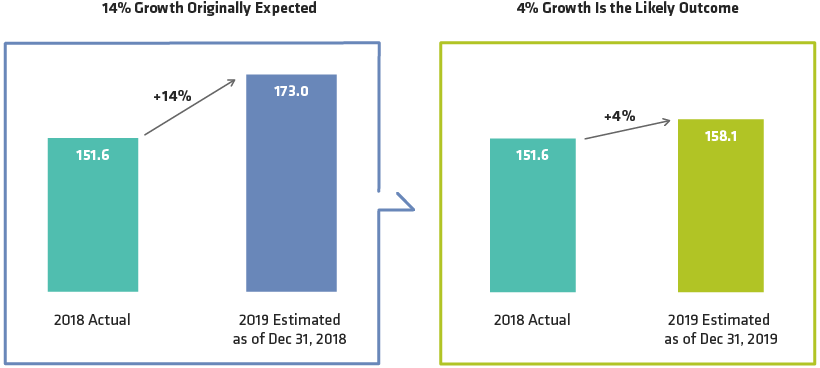

Earnings Growth Has Come Down from Initial Expectations

S&P 500: Operating Earnings per Share

Past performance and current analyses do not guarantee future results.

As of December 31, 2019

Source: S&P and AllianceBernstein (AB)

Earnings Growth and Market Performance Don’t Always Match

S&P 500: EPS Growth and Returns

Past performance and current analyses do not guarantee future results.

As of December 31, 2019

EPS: earnings per share

Source: S&P

About the Author

James T. Tierney, Jr. is Chief Investment Officer of Concentrated US Growth. Prior to joining AB in December 2013, he was CIO at W.P. Stewart & Co. Tierney began his career in 1988 in equity research at J.P. Morgan Investment Management, where he analyzed entertainment, healthcare and finance companies. He left J.P. Morgan in 1990 to pursue an MBA and returned in 1992 as a senior analyst covering energy, transportation, media and entertainment. Tierney joined W.P. Stewart in 2000. He holds a BS in finance from Providence College and an MBA from Columbia Business School at Columbia University. Location: New York

More For You

In an AI Arms Race, Investors Should Focus on Profit Potential

As the AI halo begins to fade, equity investors are seeking companies that can profit from—and not just pontificate about—artificial intelligence.

Tesla’s Troubles Signal a Speedbump for Investors in the EV Story

Competition for electric vehicles is mounting, but demand persists. So how can equity investors capture the potential of the fast-changing industry?

Concentrating on Earnings

Perspectives on Profit for Equity Investors

Earnings haven’t been consistently rewarded in equity markets recently. That could change faster than you think.