-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

The Credit Barbell Isn’t Broken. Here’s Why.

06 July 2020

5 min read

Treasuries Provide Diversification When It's Needed Most

10-Year Treasury Yield vs. High-Yield Spread: Six-Month Rolling Correlation of Daily Moves

Through May 31, 2020

High-yield spreads are option adjusted.

Source: Bloomberg Barclays and AllianceBernstein (AB)

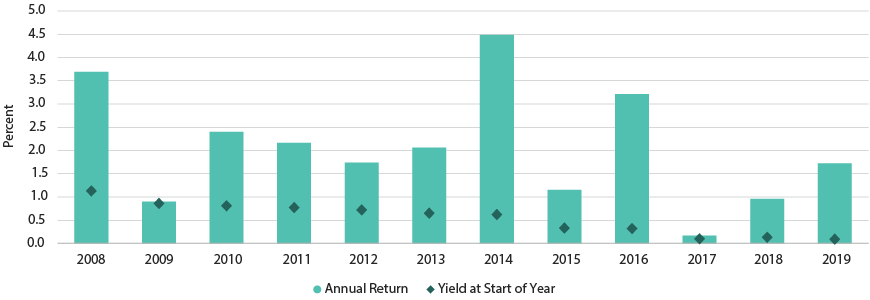

Low Yields Don't Always Mean Low Returns

10-Year Japanese Government Bonds: Yield and Return

Through December 31, 2019

Compares yield at start of year to that year's total return

Source: Bloomberg Barclays and AllianceBernstein (AB)

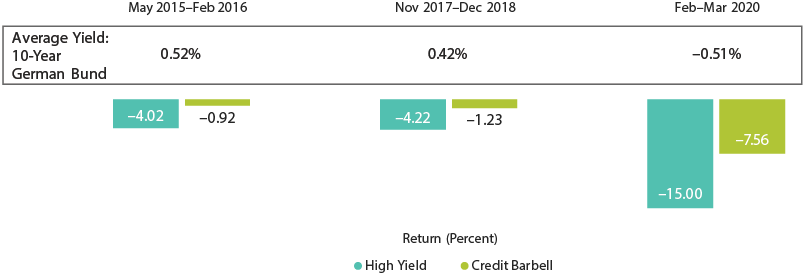

Barbell Mitigated Downside Even When Yields Were Low or Negative

Euro-Area Downturns: 2015-2020

As of June 30, 2020

High yield is represented by Bloomberg Barclays Euro High Yieuld Index; credit barbell is represented by a hypothetical naive barbell of 50% Bloomberg Barclays Euro High Yield Index and 50% 10-year German bunds.

Source: Bloomberg Barclays and AllianceBernstein (AB)

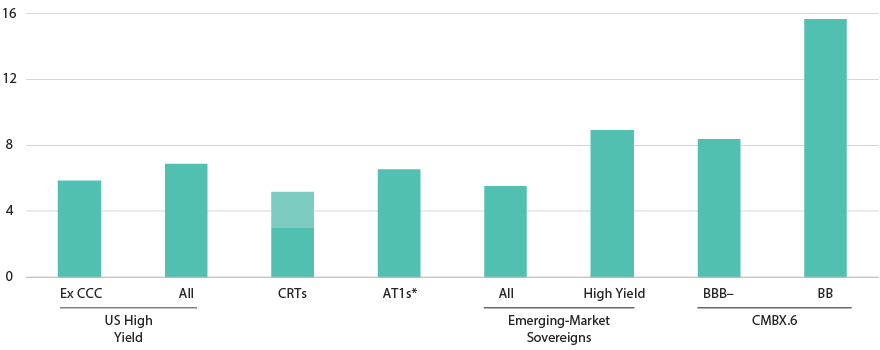

Diversifying Beyond US High YIeld Can Boost Income

Yield

CRT yields as of June 26, 2020; all other data as of June 30, 2020

*European ban AT1s

CMBX yields are loss adjusted. CRT yields are expressed as ranges.

Source Bank of America ML, Bloomberg Barclays, IHS Markit, J.P. Morgan and AllianceBernstein (AB)

About the Authors