Bonds Minus Duration

A Train Wreck in the Making?

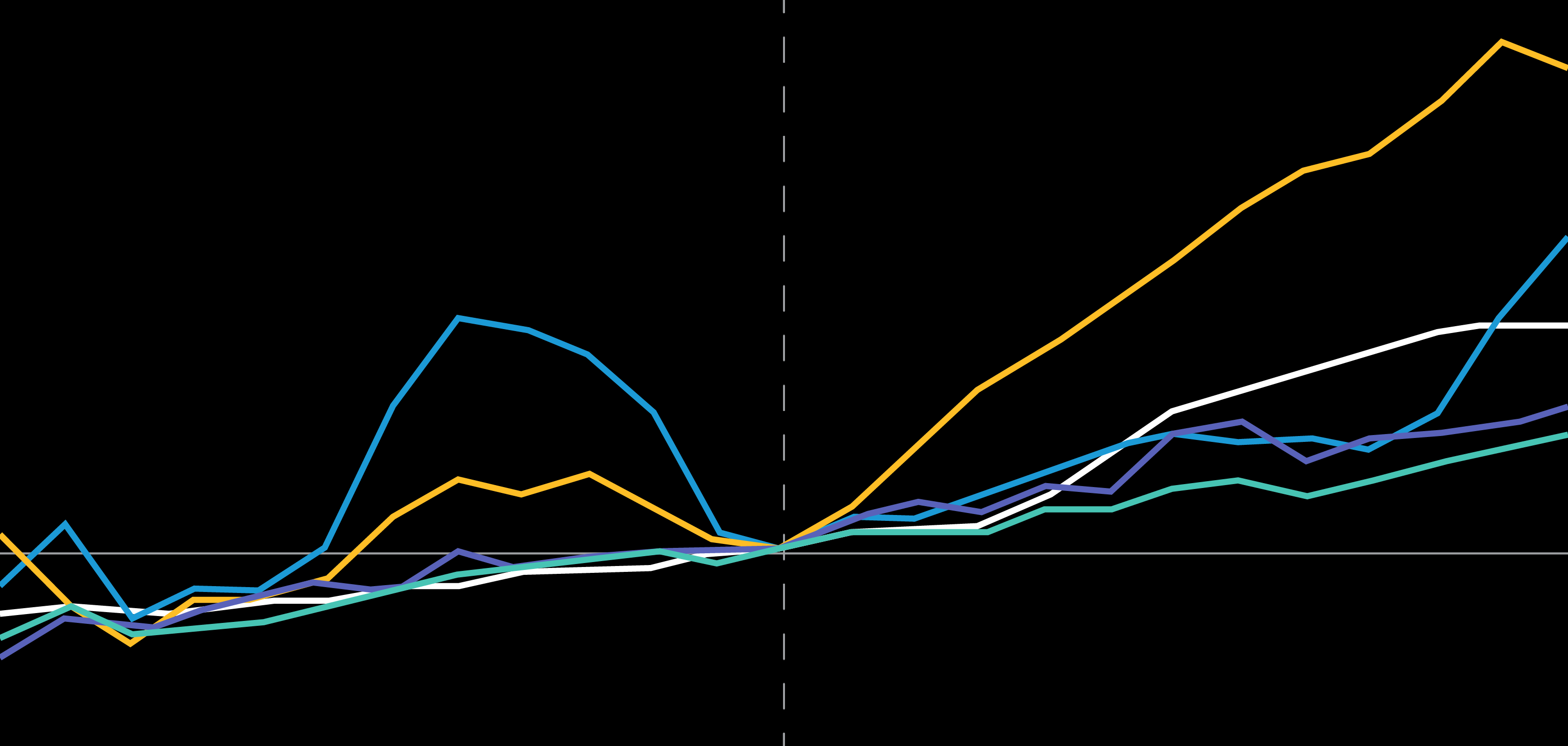

As of December 31, 2017

USHY is represented by the Bloomberg Barclays US Corporate High-Yield Index; USHY DH is represented by Bloomberg Barclays US Corporate High Yield Duration

Hedged Index; USHY—1–5 Year Index is by Bloomberg Barclays US Corporate High Yield 1–5 Year 2% Capped Index

Source: Bloomberg Barclays

As of May 28, 2018

USHY is represented by the Bloomberg Barclays US Corporate High-Yield Index; USHY DH is represented by Bloomberg Barclays US Corporate High Yield Duration

Hedged Index; USHY—1–5 Year Index is by Bloomberg Barclays US Corporate High Yield 1–5 Year 2% Capped Index

Source: Bloomberg Barclays

-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Gershon M. Distenfeld thrives on facing challenge, solving problems and putting people with different personalities and different viewpoints together to "make the engine run." When he joined AB in 1998 from a role as an operations analyst at Lehman Brothers, Distenfeld had long been fascinated by the high-yield market, and he led that practice at AB from 2006 to 2016 before assuming responsibility for all of credit. He has been co-head of fixed income since 2018.

In an industry that tends to focus on the short term, Distenfeld's investment philosophy takes the long view, considers a range of outcomes and focuses on the downside. This approach puts process and constant innovation at the forefront, making full use of AB's proprietary technology to mine the insights of fundamental and quantitative research.

"We're constantly reinventing ourselves," Distenfeld says. "We don't just sit still. We adapt to new information so we can find new factors that work."

Distenfeld's eye toward the long view extends to his charitable work with organizations like New Jersey NCSY. This youth organization for disaster relief partners with Habitat for Humanity and NECHAMA to repair homes and lives affected by natural disasters.

More For You

Investors in US fixed-income markets may want to strike while the iron is hot.

This may be the right time for multi-asset investors to consider emerging-market assets.

As normalization returns to markets in 2024, we expect inflation to return to the Fed’s target and for economic growth to moderate. Investors can still benefit from capital markets, but brace yourself for a rebalancing of asset prices.