-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Emerging-Market Debt

Putting the Fiscal House in Order

18 April 2017

3 min read

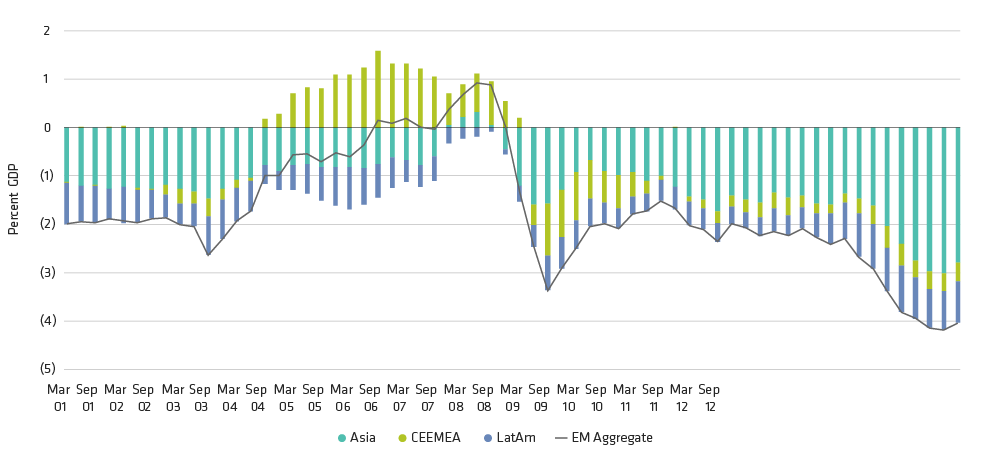

Emerging Markets' Fiscal Improvement Has Begun

EM Nominal Fiscal Balances (Including China)

Through March 31, 2017

CEEMEA = Central and Eastern Europe, Middle East and Africa

Source: Haver Analytics and AB

About the Author

Christian DiClementi is a Senior Vice President and Lead Emerging Market Debt Portfolio Manager at AB. He is also a member of the Global Fixed Income, Absolute Return and Income portfolio-management teams, and oversees emerging-market investments across AB’s suite of fixed-income products. DiClementi joined the firm in 2003. Prior to becoming a member of the Emerging Market Debt portfolio-management team in 2013, he served as a member of AB’s Economic Research Group, focusing mainly on sovereign fundamental research for the Caribbean, Central American and Latin American regions. Previously, DiClementi worked as an analyst in the firm’s Quantitative Research Group, with an emphasis on global sovereign return and risk modeling, and as an associate portfolio manager responsible for municipal bond portfolios. He holds a BS in mathematics (summa cum laude) from Fairfield University. Location: New York

More For You

Defense and Discipline: How to Stay Calm in Unruly Equity Markets

A well-planned defensive strategy can position equity portfolios to be resilient in a very harsh market environment.

European Tariff Talks: Does the US Hold All the Cards?

Negotiating with one key trade partner is tough enough. Negotiating with two is highly testing.

High-Yield Bonds: An Antidote to Volatility?

High-yield bonds may be an attractive choice for investors looking to rebalance portfolios.