Market sell-offs can be unsettling. But it’s important to keep them in perspective. The recent downturn in some credit markets is normal, given where we are in the credit cycle. It’s not evidence of a bursting bubble.

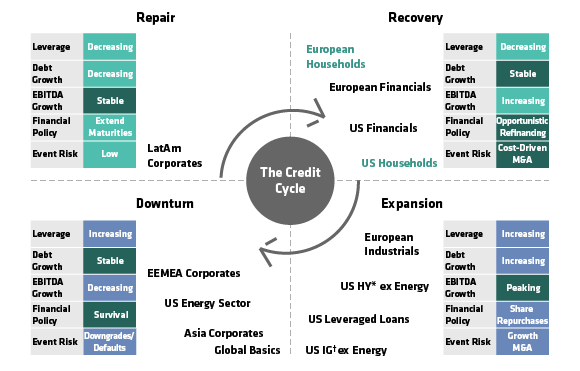

Credit cycles have distinct stages. During the expansionary period, easy access to credit helps boost earnings and prompts companies to take on debt. As those debt levels rise, so does credit risk. Asset values start to decline, causing lenders to get stingier. A rise in interest rates then usually leads to a period of contraction and balance-sheet repair and, eventually, a recovery phase.

How does this apply to what’s going on today?

Let’s look at the US high-yield market. In a recent blog, we explained why we expect defaults to rise this year—but not anywhere near as much as they did during the global financial crisis. Why? Because we don’t see this as another systemic crisis or evidence of a “high yield” bubble. This is simply what happens when the credit cycle moves from expansion into contraction.

For several years, default rates for high-yield bonds have hovered around historic lows. That was the result of rock-bottom interest rates that tempted more companies to borrow and more yield-starved investors to buy their bonds.

Another factor that drove defaults lower between 2010 and 2014 was the cleansing of the problem credits that ran into trouble following the global financial crisis.

US Energy in Contraction

Alas, nothing lasts forever. As corporate leverage rose, balance sheets started to deteriorate and lenders became more selective. Now that US interest rates have started to rise as well, many companies that binged on cheap credit no longer have such easy access to it.

High-yield energy and mining companies are already in the contraction phase of the cycle. They borrowed aggressively when commodity prices were high, only to find their margins squeezed and projects unprofitable when prices plunged. For some, bankruptcy is likely. In recent months, they’ve led the downturn in the broader US high-yield market.

Valuations in US High Yield More Attractive

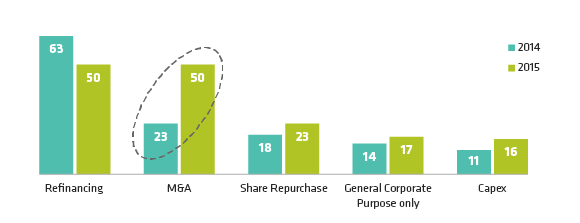

To make informed investment decisions in such volatile times, it helps to know where we are in the credit cycle. Stripped of energy-sector bonds, the US high-yield market is still in the expansion stage—but it’s getting closer to contraction. One of the clearest indicators of this is the rise in leverage to finance mergers and buyouts—a hallmark of late credit-cycle behavior (Display 1).