-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

Tackling Key Asset-Allocation Controversies

11 December 2023

5 min read

Inigo Fraser Jenkins| Co-Head—Institutional Solutions

Alla Harmsworth| Co-Head—Institutional Solutions; Head—Alphalytics

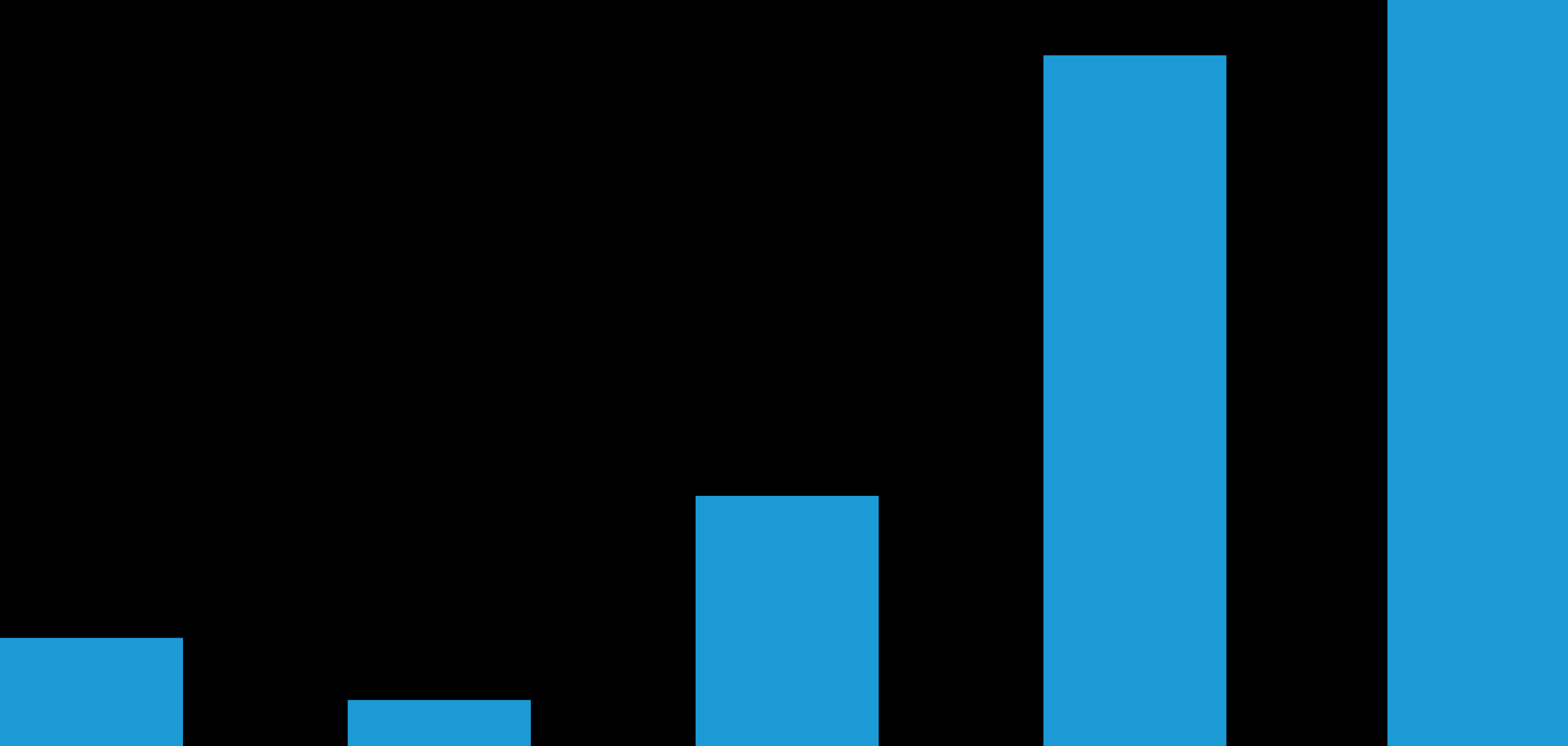

Allocations into Private Equity Appear to Be Stabilizing

Percentage of Respondents by Allocation Intention

Historical analysis and current estimates do not guarantee future results.

As of June 20, 2023

Source: Preqin and AllianceBernstein (AB)

Fixed Income Flows by Duration

USD Billions

Historical analysis does not guarantee future results.

Through October 25, 2023

Source: Emerging Portfolio Fund Research (EPFR) Global and AB

Average Pairwise Factor and Stock Correlations Are Down

Historical analysis does not guarantee future results.

Stock correlations are the average pairwise correlations of daily stock returns for constituents of the MSCI All Country World Index over a rolling six-month window.

Through August 31, 2023

Source: FactSet, MSCI, Thomson Reuters I/B/E/S and AB

China Flows Decoupling from Lackluster Rest of Emerging Markets

Equity Flows (USD Billions)

Historical analysis does not guarantee future results.

Through October 11, 2023

Source: EPFR Global and AB

About the Authors

Inigo Fraser Jenkins is Co-Head of Institutional Solutions at AB. He was previously head of Global Quantitative Strategy at Bernstein Research. Prior to joining Bernstein in 2015, Fraser Jenkins headed Nomura's Global Quantitative Strategy and European Equity Strategy teams after holding the position of European quantitative strategist at Lehman Brothers. He began his career at the Bank of England. Fraser Jenkins holds a BSc in physics from Imperial College London, an MSc in history and philosophy of science from the London School of Economics and Political Science, and an MSc in finance from Imperial College London. Location: London

Alla Harmsworth is Co-Head of Institutional Solutions and Head of Alphalytics at AB. She was previously head of European Quantitative Strategy at Bernstein Research. Prior to joining Bernstein in 2015, Harmsworth worked for two years on Nomura's Institutional Investor-ranked European Equity Strategy and Quantitative Strategy team. Her previous experience includes seven years at Fidelity as a quantitative analyst and portfolio manager, along with stints at Nikko Asset Management and ABN AMRO. Harmsworth holds a BA (Hons) and an MA in philosophy, politics and economics from University College Oxford and an MSc in economics from the London School of Economics and Political Science. Location: London

More For You

Why Does Volatility Often Lead to Strong Emerging Equity Returns?

Emerging-market stocks have done particularly well after equity market crises in the past.

Where Do Private Assets Fit in an Insurer’s Liability Profile?

The wide range of private assets has a lot to offer insurance investors, in our view.

What Raising the Trade Drawbridge Means for the World Economy

Trade wars threaten longstanding trade partnerships and could weigh on the global economy.