-

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

Why Fallen Angels Can Be a Good Catch

22 May 2020

1 min read

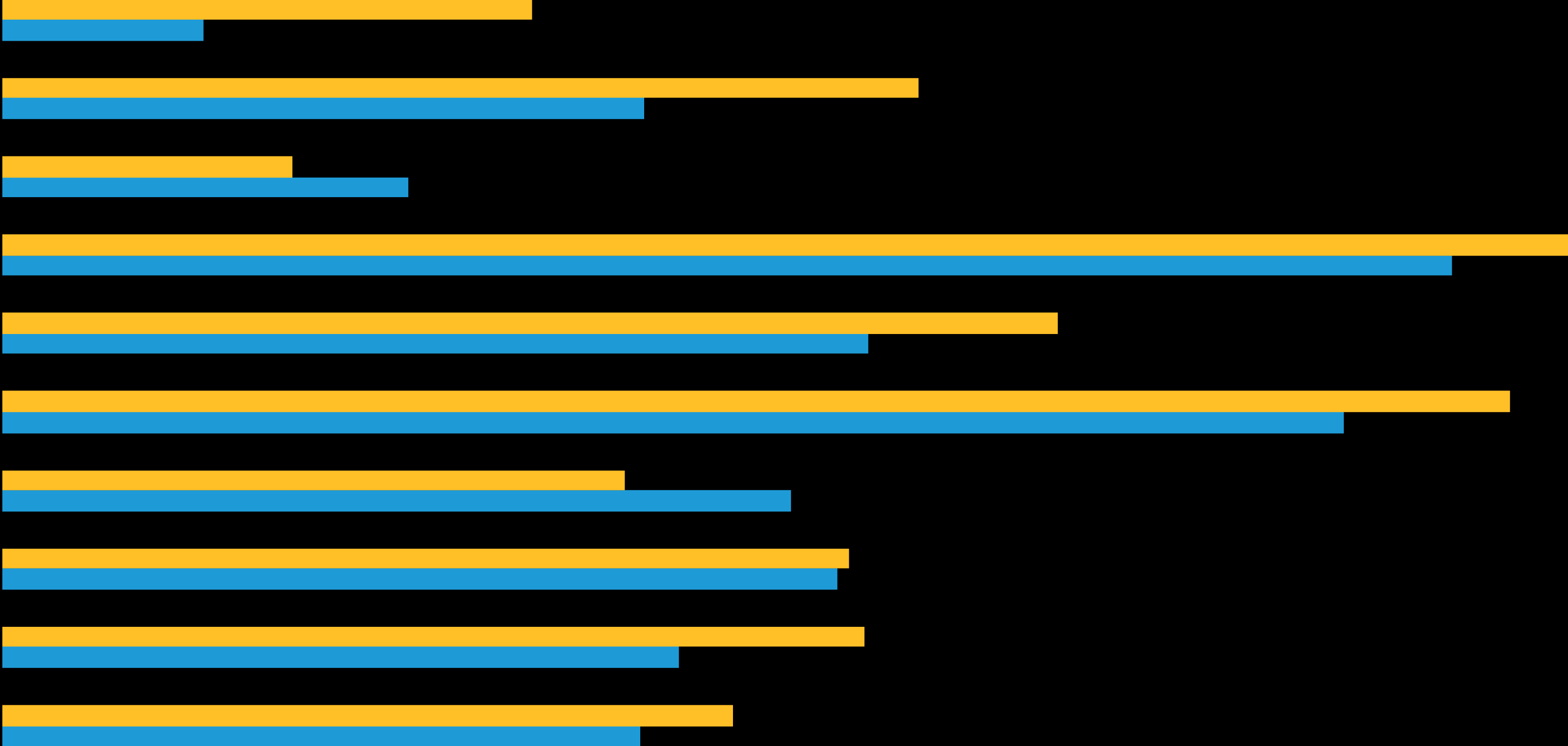

An Expected Surge in Fallen angels: The More, The Merrier

Historical analysis does not guarantee future results.

As of March 31, 2020

US Corporation represented by Bloomberg Barclays US Corporate

Source: Bloomberg Barclays, ICE BofA, JP Morgan, Moody’s and AllianceBernstein (AB)

More For You

Capital Markets Outlook 2Q 2025: At the Intersection of Fear and Hope

After a disappointing quarter and a bout of tariff turmoil, what does the opportunity set look like?

Anatomy of a US Treasury Sell-Off

What triggered April’s Treasury sell-off? What’s next? And how should investors manage duration risk?

Gauging the Fear Factor: From Volatility Peaks to Equity Returns

Extreme fear in equity markets has often been followed by extremely good returns.