-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

- Institutional Investor

- Investment Professional

- Individual Investor

The Norway website is not available. You will be redirected to the Luxembourg website which contains funds approved for marketing in Luxembourg, and where several of these funds are not registered for marketing in Norway.

Norges nettside er ikke tilgjengelig. Du vil bli omdirigert til Luxembourg-nettstedet som inneholder midler godkjent for markedsføring i Luxembourg, og hvor flere av disse fondene ikke er registrert for markedsføring i Norge.

Emerging-Market Stocks: Great Businesses Hide in a Murky Market Landscape

25 June 2024

5 min read

Greek Banks Are on the Road to Recovery After a Tough Decade

Past performance and current analysis do not guarantee future results

As of December 31, 2023

Source: Bank of Greece and Bloomberg

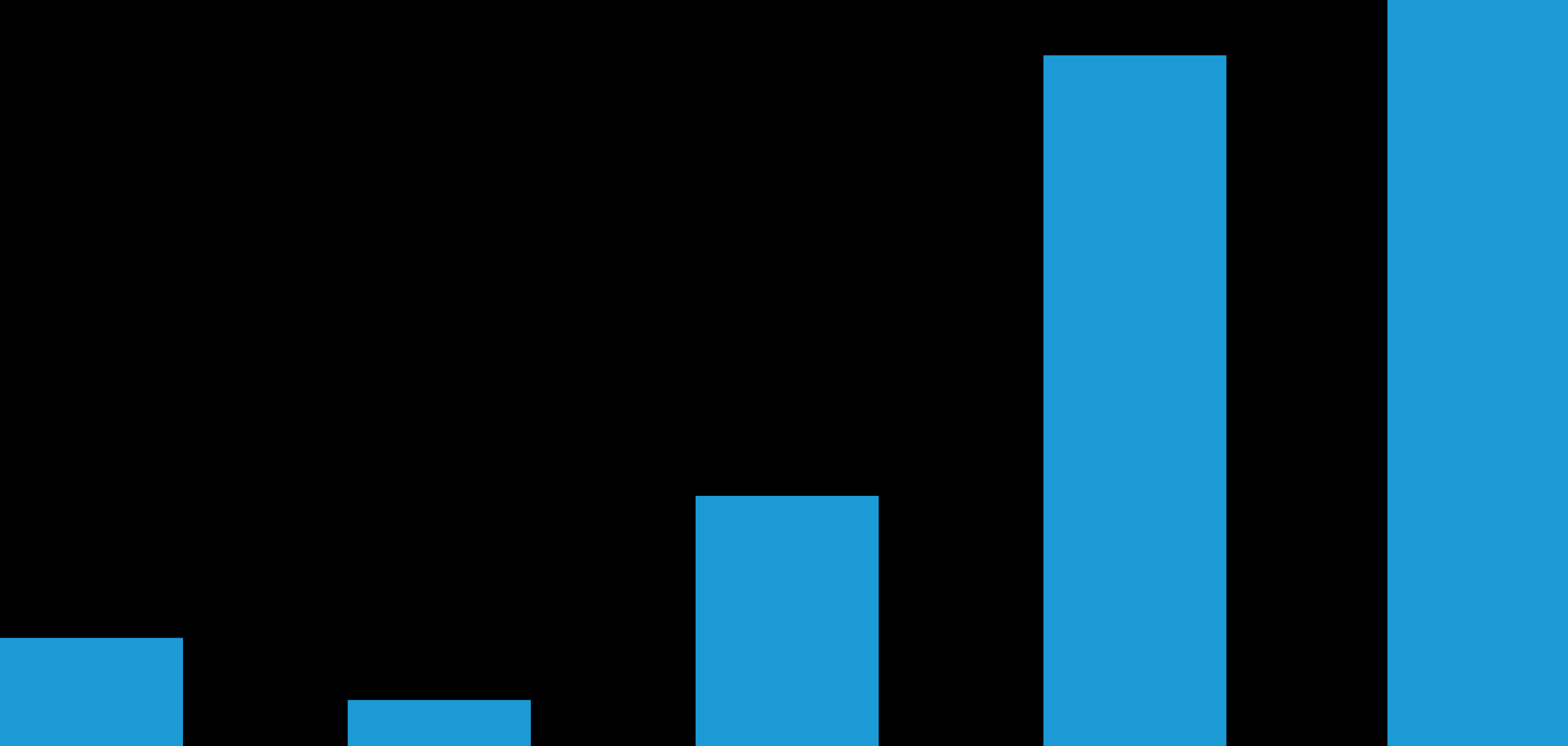

Many South Korean Companies Trade at Persistently Cheap Valuations

Percent of Companies Valued at Less than 1x Price-to-Book

Current analysis and forecasts do not guarantee future results.

South Korea represented by KOSPI 200, Japan by TOPIX, Europe by STOXX 600 and US by S&P 500.

As of March 31, 2024

Source: FactSet and Goldman Sachs Global Investment Research

-

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

-

References to specific securities discussed are for illustrative purposes only and should not to be considered recommendations by AllianceBernstein L.P. It should not be assumed that investments in the securities mentioned have necessarily been or will necessarily be profitable.

About the Author

Sammy Suzuki is Head of Emerging Markets Equities, responsible for overseeing AB’s emerging-markets equity business and instrumental in the formation and shaping of AB’s Emerging Markets Equity platform. He was also a key architect of the Strategic Core platform and has managed the Emerging Markets Portfolio since its inception in 2012, and the Global, International and US portfolios from 2015 to 2023. Suzuki has managed portfolios since 2004. From 2010 to 2012, he also held the role of director of Fundamental Value Research, where he managed 50 fundamental analysts globally. Prior to managing portfolios, Suzuki spent a decade as a research analyst. He joined AB in 1994 as a research associate, first covering the capital equipment industry, followed by the technology and global automotive industries. Before joining the firm, Suzuki was a consultant at Bain & Company. He holds both a BSE (magna cum laude) in materials engineering from the School of Engineering and Applied Science, and a BS (magna cum laude) in finance from the Wharton School at the University of Pennsylvania. Suzuki is a CFA charterholder and was previously a member of the Board of the CFA Society New York. He currently serves on the Board of the Association of Asian American Investment Managers. Location: New York

More For You

Chinese Equities: Investing in Stocks That Transcend Tariff Turmoil

They may be the main target of US tariffs, but many Chinese companies can cope with trade-war pressures.

Anatomy of a US Treasury Sell-Off

What triggered April’s Treasury sell-off? What’s next? And how should investors manage duration risk?

Why Does Volatility Often Lead to Strong Emerging Equity Returns?

Emerging-market stocks have done particularly well after equity market crises in the past.