-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Portfolio Risk Management

A Multidimensional Perspective

23 September 2019

10 min read

Daniel Loewy, CFA| Chief Investment Officer and Head—Multi-Asset and Hedge Fund Solutions

Sharat Kotikalpudi| Director of Quantitative Research—Multi-Asset Solutions

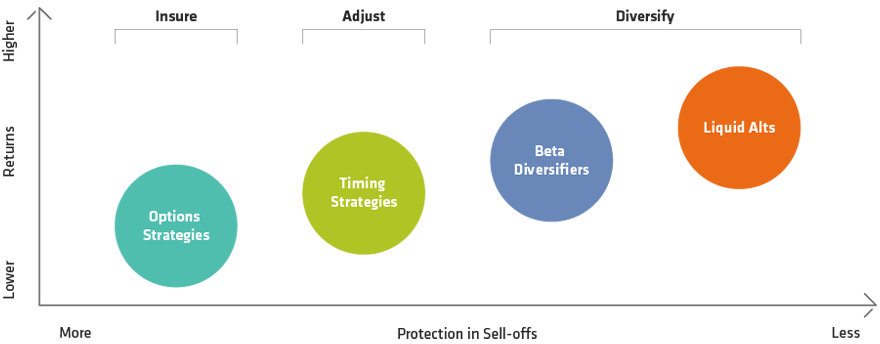

Portfolio Risk-Management Tools

Source: AllianceBernstein (AB)

How Do Risk-Management Tools Fare When Equities Falter?

Return of Tools by Equity Performance Decile

Through June 28, 2019

Timing Equity Using Volatility represents the return of a strategy that takes long or short developed equity market positions based on volatility. If volatility is higher than usual, the strategy shorts equity, and vice versa. Volatility is measured by a proprietary risk model. Results are based on simulated daily returns from December 9, 1971, through June 28, 2019. Commodities are based on the Bloomberg Commodity Index starting in 1991 and on AB data prior to 1991. Returns are from December 6, 1971, through June 28, 2019. Yen is based on the simulated return of a constant three-month forward Yen/Dollar forward contract—they include spot currency movements and carry. Yen returns are from September 1, 1978, through June 28, 2019. Equity return deciles are based on developed-market daily excess returns from December 6, 1971, to June 28, 2019.

Source: Bloomberg and AllianceBernstein (AB)

Risk-Management Tools: A Historical Perspective

Through June 28, 2019

Protection is measured by the correlation of a tool to developed market equity excess returns, using overlapping five-day returns starting from December 6, 1971, or the start date of the underlying strategy, whichever is later, through June 28, 2019. Return represents a proprietary risk-adjusted return score that incorporates effectiveness, reliability and length of history. The score equals the average of the full-period and five-year half-life weighted decay-weighted Sharpe ratio divided by the standard error of the rolling six-month Sharpe ratio. The size of the circles is proportional to the hit rate of protection—the percentage of days that the strategy produced positive returns when equity market excess returns were lower than –1%.

*CTA denotes Commodity Trading Advisors, a strategy that invests in financial assets based on their historical trends. It is represented by the NEIXCTAT Index of 10 equal-weighted trend-following CTAs

Source: AllianceBernstein (AB)

A Closer Look at Timing Strategies

Through June 28, 2019

Protection is measured by the correlation of a tool to developed-market equity excess returns, using overlapping five-day returns starting from December 6, 1971, or the start date of the underlying strategy, whichever is later, through June 28, 2019. Return represents a proprietary risk-adjusted return score that incorporates effectiveness, reliability and length of history. The score equals the average of the full-period and five-year half-life weighted decay-weighted Sharpe ratio divided by the standard error of the rolling six-month Sharpe ratio. The size of the circles is proportional to the hit rate of protection—the percentage of days that the strategy produced positive returns when equity market excess returns were lower than –1%.

Source: AllianceBernstein (AB)

A Closer Look at Beta Diversifiers

Through June 28, 2019

Protection is measured by the correlation of a tool to developed-market equity excess returns, using overlapping five-day returns starting from December 6, 1971, or the start date of the underlying strategy, whichever is later, through June 28, 2019. Return represents a proprietary risk-adjusted return score that incorporates effectiveness, reliability and length of history. The score equals the average of the full-period and five-year half-life weighted decay-weighted Sharpe ratio divided by the standard error of the rolling six-month Sharpe ratio. The size of the circles is proportional to the hit rate of protection—the percentage of days that the strategy produced positive returns when equity market excess returns were lower than –1%.

Source: AllianceBernstein (AB)

About the Authors

Daniel Loewy is Chief Investment Officer and Head of Multi-Asset and Hedge Fund Solutions. He oversees the research and product design of the firm’s multi-asset strategies, as well as their implementation. In addition, Loewy is Chief Investment Officer for Dynamic Asset Allocation, and is responsible for the development and investment decision-making for that service. He is also a member of the Real Asset Investment Policy Group and the Target Date Investment Oversight team. Loewy previously led the Wealth Management Group’s research on the major investment issues faced by our highest-net-worth clients, including asset allocation, alternative investments and tax management. Prior to that, he was a research analyst in the equity research department, where he followed the aerospace and defense and capital goods sectors. Additionally, Loewy has served as an associate portfolio manager for our value equity services. He holds a BS in industrial and labor relations from Cornell University and an MBA from Columbia University, and is a CFA charterholder. Location: New York

Sharat Kotikalpudi is the Director of Quantitative Research in the Multi-Asset Solutions Group at AB, specializing in systematic macro strategies; he leads the group's quantitative research in directional and cross-sectional strategies across developed and emerging markets within equity futures, currencies, rates and commodities. He is also a Portfolio Manager of AB Systematic Macro. Kotikalpudi joined AB in 2010 as a quantitative analyst on the Dynamic Asset Allocation team, where he helped to design and develop the quantitative toolset used in the group’s asset-allocation strategies. He holds a BE in electronics and communication engineering from the Manipal Institute of Technology, India, an MA in mathematics of finance from Columbia University and a PGDM from the Indian Institute of Management Calcutta. Location: New York

More For You

World Economy to Continue Rebalancing in 2025

The range of potential economic outcomes is wide, but a solid starting point suggests resilience.

Mapping Out the 2025 Investment Landscape Across Asset Classes

Global markets will face powerful disruptive forces next year. How can investors prepare in fixed-income, equity and alternative investment strategies?

Five Themes for ’25 and their SAA Implications for US Equities, TIPS and Crypto

This note outlines five investment themes for 2025. These are not necessarily trades for the coming year, but rather issues that asset owners need to think about—even if some implications are longer term. They are topics which we believe necessitate a change in investors’ expectations and in their asset allocations.