-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

Looking to De-Risk? High Yield Can Help

29 April 2019

2 min read

Gershon M. Distenfeld, CFA | Director—Income Strategies

Will Smith, CFA| Director—US High Yield

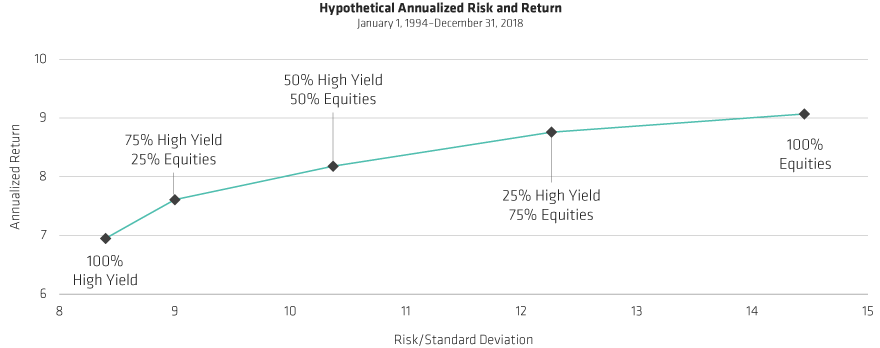

High-Yield Bonds and Equities: Effective Complements

A Combination of High Yield* and Equities† Has Historically Improved Risk-Adjusted Returns

As of December 31, 2018.

Past performance is not a guarantee of future results. There can be no assurance that an actual portfolio based on the hypothetical portfolio underlying the above illustration could be created or, if created, that it would achieve the results implied above or be profitable.

Diversification does not illuminate risk of loss.

*Based upon a hypothetical portfolio; accordingly, such performance is not based upon historical performance of any investment portfolio. This illustration is not intended to provide either a complete analysis regarding any or all of the variables that could affect any particular portfolio. High-yield is represented by Bloomberg Barclays US corporate high-yield.

†Equities is represented by S&P 500 index. All indices cited hearing are used for purposes of comparison purposes only. An investor generally cannot invest directly in an index, and its performance does not reflect the performance of any AB portfolio.

Source: Bloomberg Barclays, S&P and AllianceBernstein (AB)

About the Authors

Gershon Distenfeld is a Senior Vice President, Director of Income Strategies and a member of the firm’s Operating Committee. He is responsible for the portfolio management and strategic growth of AB’s income platform with almost $60B in assets under management. This includes the multiple-award-winning Global High Yield and American Income portfolios, flagship fixed-income funds on the firm’s Luxembourg-domiciled fund platform for non-US investors. Distenfeld also oversees AB’s public leveraged finance business. He joined AB in 1998 as a fixed-income business analyst and served in the following roles: high-yield trader (1999–2002), high-yield portfolio manager (2002–2006), director of High Yield (2006–2015), director of Credit (2015–2018) and co-head of Fixed Income (2018–2023). Distenfeld began his career as an operations analyst supporting Emerging Markets Debt at Lehman Brothers. He holds a BS in finance from the Sy Syms School of Business at Yeshiva University and is a CFA charterholder. Location: Nashville

Will Smith is a Senior Vice President and Director of US High Yield Credit. He is also a member of the High Income, Global High Yield, Limited Duration High Income, Short Duration High Yield and European High Yield portfolio-management teams. Smith designed and is one of the lead portfolio managers for AB’s Multi-Sector Credit Strategy, which invests across investment-grade and high-yield credit sectors globally. He leads the monthly High Yield portfolio-construction meeting, and is a member of the Credit Research Review Committee, which determines investment policy for the firm’s credit-related portfolios. Smith has authored several papers and blogs on high-yield investing, including one on the importance of using a probability-based framework to build better portfolios. He joined AB in 2012, and spent 2014 in London as part of the European High Yield portfolio-management team. Smith started his career with UBS Investment Bank, working as an analyst with the Credit Risk team and then later on the Fixed Income sales and trading desk. He holds a BA in economics from Boston College and is a CFA charterholder. Location: Nashville

More For You

Emerging-Market Equities: The Steep Cost of Missing Out

Staying invested in EM stocks can help avoid sacrificing attractive return potential.

What is a Defensive Trade Today?

Low Vol vs. Quality vs. Bonds vs. Gold

With more investors looking for defensive trades, what counts as a defensive trade in today’s environment? Differences in valuation—and different interpretations of what counts as defensive—mean that not all such trades are equal.

What’s on Insurers’ Minds: Insights from Industry Leaders

Though geopolitics has come to the fore, insurers are addressing a wide range of other issues.