The media and some market observers are bracing for a blizzard of BBB-rated bonds to get downgraded to junk as the credit cycle turns. We expect it will be closer to a flurry.

Investors are right to be concerned, of course. US corporate debt surged when interest rates were low. And companies at the bottom of the investment-grade credit ladder were among the biggest borrowers.

BBB bonds accounted for nearly half the US investment-grade index when 2018 began, from about 33% in late 2008. Excluding financial issuers (whom regulators have forced to deleverage since the crisis), BBBs went from 52% in 2008 to 57% in this year.

It’s important to remember, though, that not all BBB-rated bonds are the same. Investors who can separate the strong from the weak before the credit rating agencies act may be able to improve their return potential.

Rising Rates, Rising Anxiety

BBB credits are in the spotlight now because rising rates and inflation are pushing up firms’ financing and input costs, squeezing profit margins. Some investors worry that billions of dollars’ worth of debt could tumble to junk, locking in losses for anyone who owns these “fallen angels,” as ex-high-grade bonds are known. A mass downgrade to junk would spark disruptive repricing in the high-yield market, too.

We understand why these concerns are keeping some bond investors up at night. But it’s important to keep things in perspective. Will some issuers lose their investment-grade status? Of course. But predicting when is difficult. The process for many could take years to play out, especially with the US economy still likely to grow in 2019.

Based on our credit analysis and expectation for continued—if slower—US growth next year, we estimate that a small percentage of the investment-grade market is at risk of a downgrade to high yield, and not all at once.

That’s not insignificant. But it’s hardly a blizzard.

Not All BBBs Are Created Equal

The problem, as we see it, is that the market hasn’t been doing a great job of factoring the differences among BBB issuers into how their bonds are priced. This is largely because the rating agencies have so far given companies a lot of leeway when it comes to maintaining an investment-grade rating—even when the credit metrics say they should be high yield. In many cases, the agencies have given companies credit for deleveraging plans that have yet to become reality.

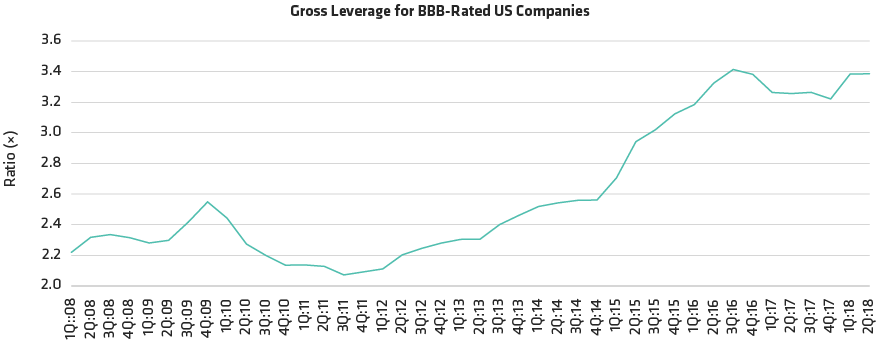

Nearly every company in the index took on more leverage over the last decade when interest rates were at record lows, with the median gross leverage for BBB-rated industrials rising from 2.2 times earnings in 2008 to nearly 3.4 times in mid-2018 (Display). That paved the way for some to misallocate capital. Now, with rates rising and liquidity scarcer, firms that misused their capital are slowly being exposed.