-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Why EM Corporate Debt Deserves a Place in Your Portfolio

03 September 2019

4 min read

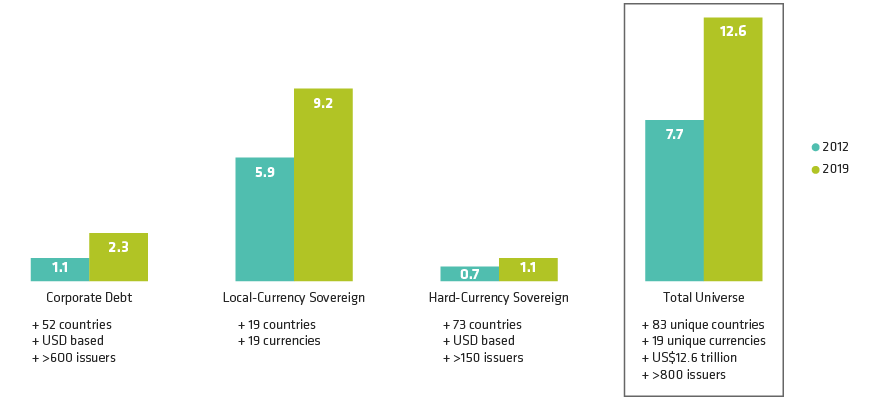

A Bigger Pond to Fish In: EM Debt’s Growing Opportunity Set

Total Debt Stock (USD Trillions)

As of June 30, 2019

For informational purposes only. There can be no assurance that any investment objectives will be achieved.

Corporate Debt: J.P. Morgan CEMBI Broad Diversified; Local-Currency Sovereign: J.P. Morgan GBI-EM Global Diversified; Hard-Currency Sovereign: J.P. Morgan EMBI

Global Diversified

Source: J.P. Morgan Markets and AllianceBernstein (AB)

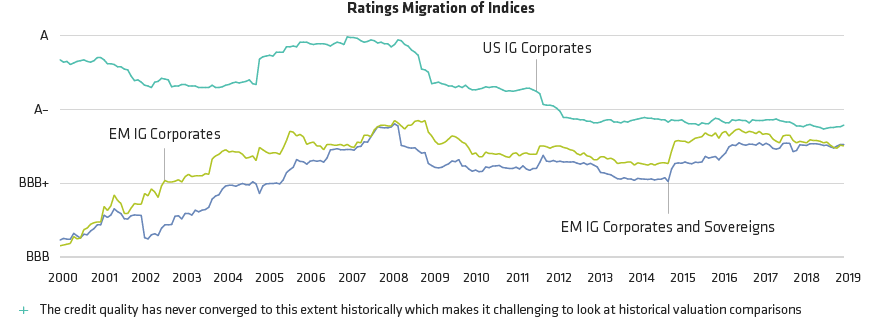

Not Much Difference Between EM and US Corporate Credit Quality

Through May 31, 2019

Source: Bank of America Merrill Lynch and AllianceBernstein (AB)

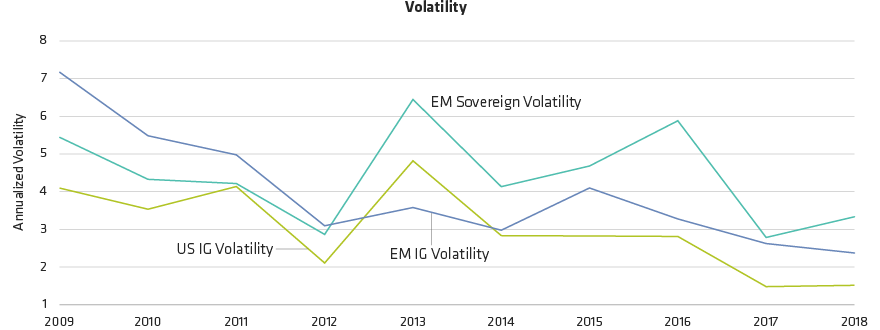

Smoother Ride: High-Quality EMD Has Become Less Volatile

As of December 31, 2018

Historical and current analyses do not guarantee future results.

Annualized volatility is shown for the J.P. Morgan EMBI Global-Investment, Grade, J.P. Morgan CEMBI Broad Investment Grade, and J.P. Morgan US Liquid (JULI)

Investment-Grade indices.

Source: Bloomberg Barclays and J.P. Morgan Markets

About the Author