-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

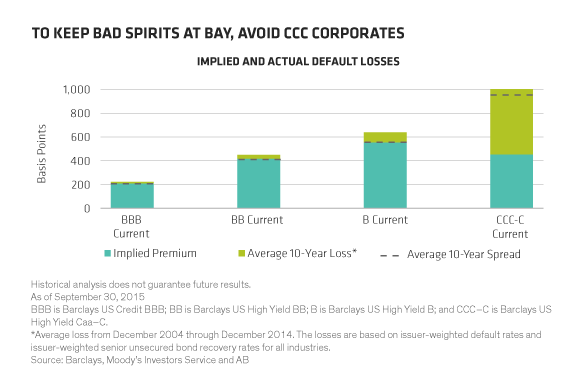

To Keep Bad Spirits at Bay, Avoid CCC Corporates

Oct 27, 2015

2 min read

About the Author