-

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

Global Stocks: Look Beyond Home Base to Find Growth

Nov 28, 2022

6 min read

The Source of Company Revenues Can Affect Investing Returns

Past performance and current analysis do not guarantee future results.

*Europe represented by STOXX 600 Index, Japan by TOPIX, US by S&P 500 and emerging markets by MSCI Emerging Markets

†Equal-weighted returns for S&P 500 constituents grouped by percentage of revenues derived from non-US business

Left chart as of December 31, 2021; right chart as of September 30, 2022

Source: Bloomberg, FactSet, Goldman Sachs Global Investment Research, MSCI, S&P, STOXX, TOPIX, and AllianceBernstein (AB)

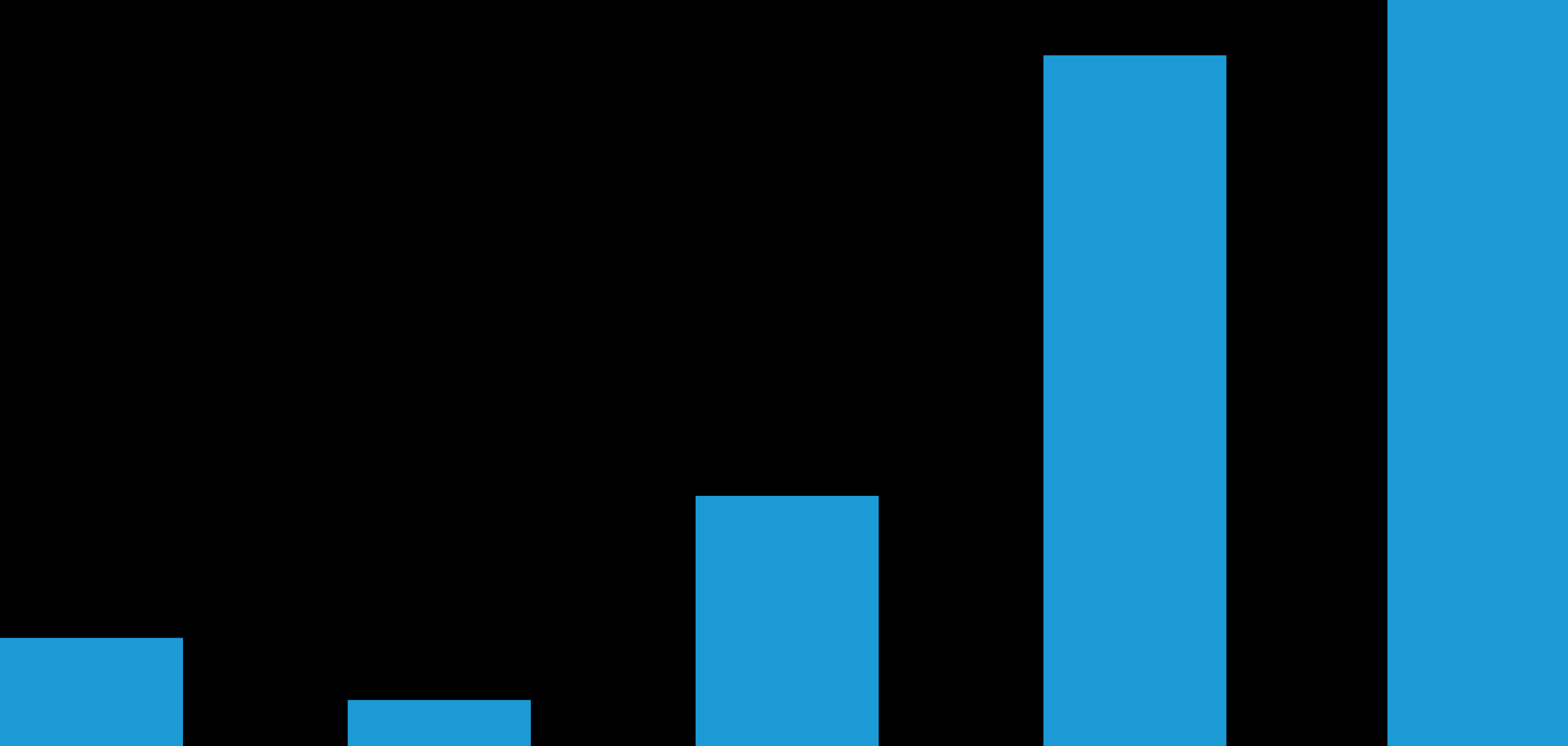

Earnings Revisions Appear to Reflect International Exposures

Past performance and current analysis do not guarantee future results.

*Domestic focus (GSTHAINT) includes an equal-weighted group of 50 S&P 500 stocks with the highest domestic exposure using 2021 company filings. International focus (GSTHINTL) includes an equal-weighted group of 50 S&P 500 stocks with the highest international sales exposure based on 2021 company filings.

†US exposure (GSSTAMER) includes an equal-weighted group of 45 European companies with US sales exposure above market average and negative correlation with the EUR/USD exchange rate. Domestic exposure (GSSTDOME) includes an equal-weighted group of 60 European companies with a high euro-area sales exposure. UK domestic exposure (GSSTUKDE) includes an equal-weighted group of 35 UK companies with high sales exposure to the UK.

Left chart as of October 28, 2022. Right chart as of October 14, 2022.

Source: Datastream, FactSet, Goldman Sachs Global Investment Research and Thomson Reuters I/B/E/S

-

References to specific securities are presented to illustrate the application of our investment philosophy only and are not to be considered recommendations by AB. The specific securities identified and described do not represent all of the securities purchased, sold or recommended for the portfolio, and it should not be assumed that investments in the securities identified were or will be profitable.

About the Authors

Dev Chakrabarti is a Senior Vice President and Chief Investment Officer for Concentrated Global Growth. Prior to joining AB in December 2013, he was a portfolio manager/analyst on the global equity research and portfolio-management team at WPS Advisors. Chakrabarti joined W.P. Stewart in 2005 as a member of the European equity research and portfolio-management team and moved to New York in 2008 to focus on global portfolios. Earlier in his career, he worked as an M&A analyst at Merrill Lynch, a financial analyst at Unilever and an equity analyst at J.P. Morgan Securities, where he specialized in European technology stocks. Chakrabarti holds a BSc (Hons) in economics from the University of Bristol and an MSc in finance from London Business School. Location: London

More For You

Anatomy of a US Treasury Sell-Off

What triggered April’s Treasury sell-off? What’s next? And how should investors manage duration risk?

Why Does Volatility Often Lead to Strong Emerging Equity Returns?

Emerging-market stocks have done particularly well after equity market crises in the past.

How Tariff Troubles May Hurt Europe’s Growth

President Trump’s tariffs bring déjà vu for the euro-area economy: it’s back to slower growth and lower rates.