-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

Fixed-Income Midyear Outlook: Sail with the Tide

Jul 01, 2024

4 min read

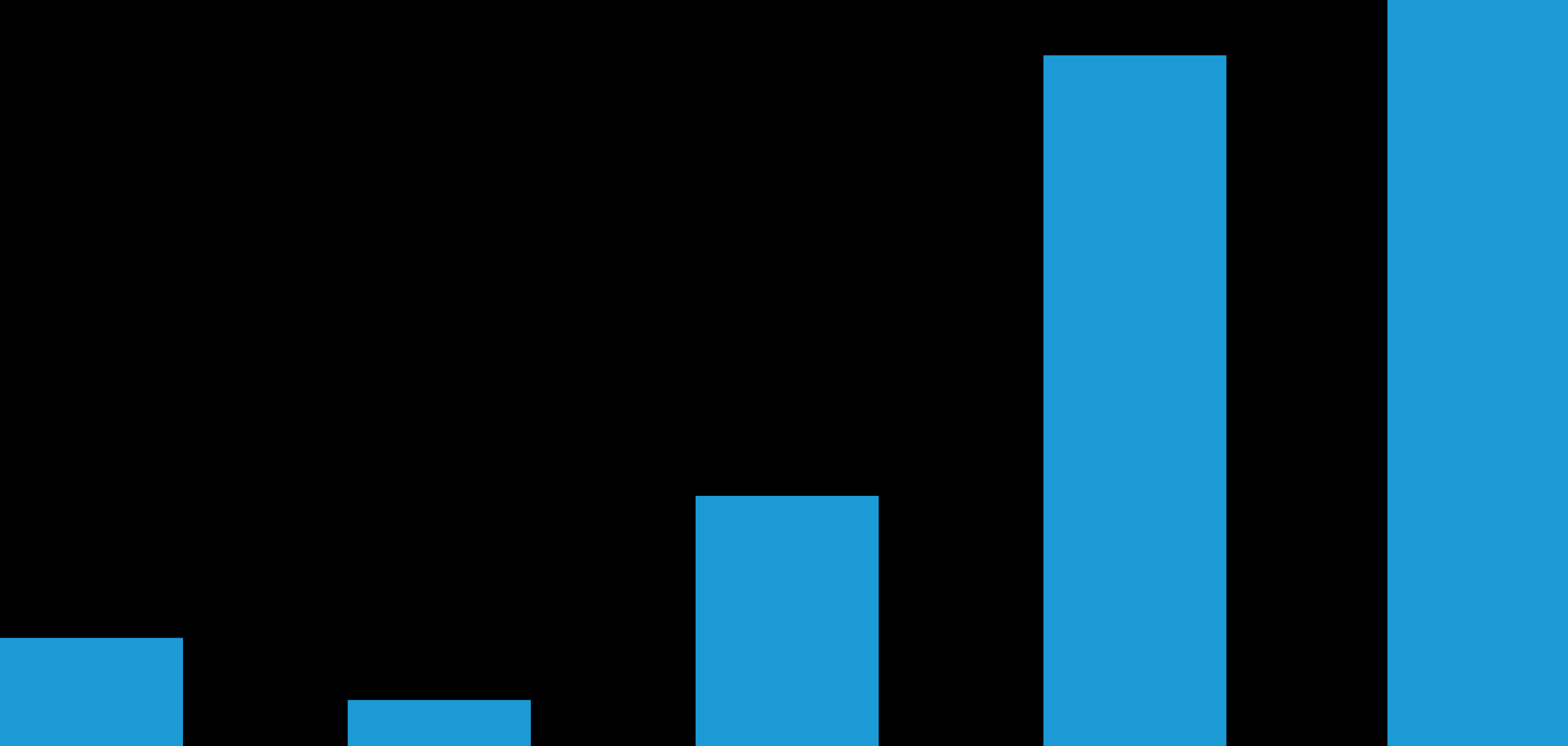

Historically, Early Birds Enjoyed the Strongest Bond Market Returns

Bloomberg US Aggregate Bond Index: Average 12-Month Forward Return (Percent)

Historical analysis does not guarantee future results.

Average is based on the following dates of first Fed rate cuts: September 20, 1984; June 7, 1989; July 6, 1995; January 3, 2001; September 18, 2007; and August 1, 2019.

As of December 31, 2023

Source: Bloomberg, US Federal Reserve and AllianceBernstein (AB)

About the Authors

Scott DiMaggio is a Senior Vice President, Head of Fixed Income and a member of the Operating Committee. As Head of Fixed Income, he is responsible for the management and strategic growth of AB’s fixed-income business and investment decisions across the department. DiMaggio has previously served as director of Global Fixed Income and continues to be a portfolio manager across numerous multi-sector and multi-currency strategies. Prior to joining AB’s Fixed Income portfolio-management team, he performed quantitative investment analysis, including asset-liability, asset-allocation, return attribution and risk analysis for the firm. Before joining the firm in 1999, DiMaggio was a risk management market analyst at Santander Investment Securities. He also held positions as a senior consultant at Ernst & Young and Andersen Consulting. DiMaggio holds a BS in business administration from the State University of New York, Albany, and an MS in finance from Baruch College. He is a member of the Global Association of Risk Professionals and a CFA charterholder. Location: New York

More For You

Anatomy of a US Treasury Sell-Off

What triggered April’s Treasury sell-off? What’s next? And how should investors manage duration risk?

Why Does Volatility Often Lead to Strong Emerging Equity Returns?

Emerging-market stocks have done particularly well after equity market crises in the past.

How Tariff Troubles May Hurt Europe’s Growth

President Trump’s tariffs bring déjà vu for the euro-area economy: it’s back to slower growth and lower rates.