-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Considering High-Yield Bank Loans? Proceed With Caution

Dec 09, 2016

3 min read

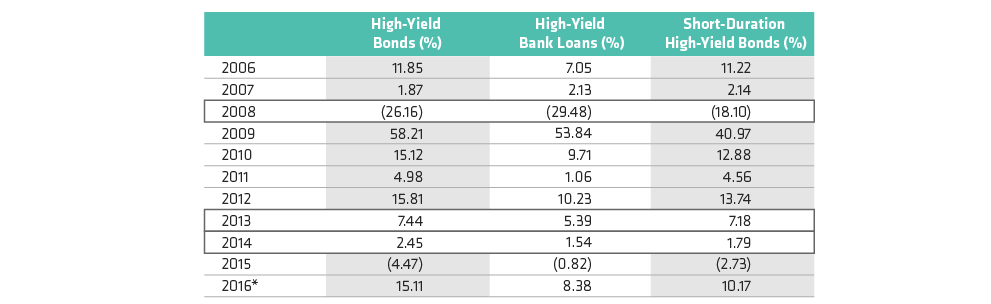

Bonds Beat Bank Loans, Even During Tough Years

As of September 30, 2016

High-yield bonds are represented by Bloomberg Barclays US Corporate High-Yield; high-yield bank loans by Bloomberg Barclays US High-Yield Loans; short-duration high-yield bonds by Bloomberg Barclays US High-Yield Ba/B 1–5 Year

*Through September 30, 2016

Source: Bloomberg Barclays

About the Author