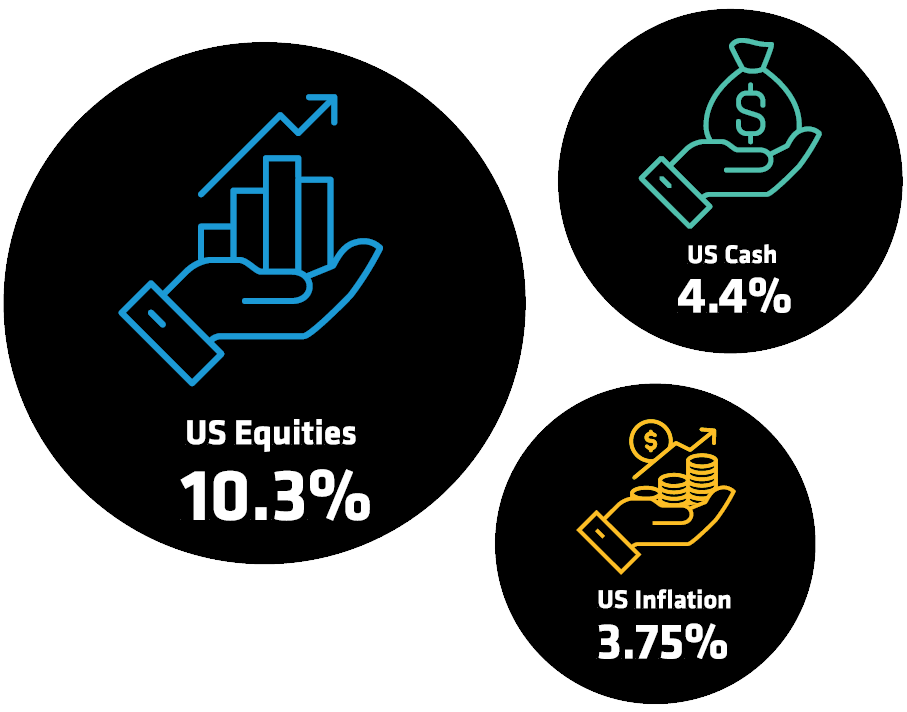

Money-Market Funds have Been the Clear Favorite

Historical analysis does not guarantee future results.

As of September 11, 2024 | Source: EPFR and AB